MB Stories

Biochemistry reimagined – Where reagents, analyzers, and intelligence converge

Biochemistry instruments and reagents form the analytical backbone of laboratory diagnostics, driving accuracy from basic assays to advanced clinical decision-making.

The biochemistry analyzer market is in the midst of a long, sustained growth cycle driven by the convergence of chronic disease burden, structural upgrades in healthcare infrastructure, and rapid advances in automation, connectivity, and data intelligence. What was once a largely hardware driven, routine chemistry segment has now evolved into a strategically important pillar of in vitro diagnostics, tightly integrated with hospital information systems, laboratory automation lines, and increasingly with AI enabled analytics. As a result, biochemistry analyzers are no longer viewed simply as instruments that produce numerical results, but as central platforms that shape clinical workflows, inform care pathways, and influence overall health system efficiency.

Indian market dynamics

Within this global picture, the Indian market is emerging as one of the most dynamic arenas for biochemistry analyzers, sitting at the intersection of rising disease burden, aggressive diagnostic expansion, and strong policy focus on domestic manufacturing. Rapid growth in organized diagnostic chains, the expansion of tertiary care hospitals, and government led initiatives around insurance coverage and public health screening are collectively driving up test volumes and sharpening expectations around quality and turnaround time. Laboratories are moving away from fully manual or basic semi automated systems toward modern automated analyzers, often skipping intermediate generations of technology and adopting cloud connected, LIS integrated platforms that align with broader digital health programs. At the same time, India’s emphasis on “Make in India” and self reliance in medical devices is creating space for local and regional manufacturers to compete with global majors, especially in segments such as mid range analyzers, reagents adapted to local conditions, and service intensive offerings tailored to tier-II and tier-III cities.

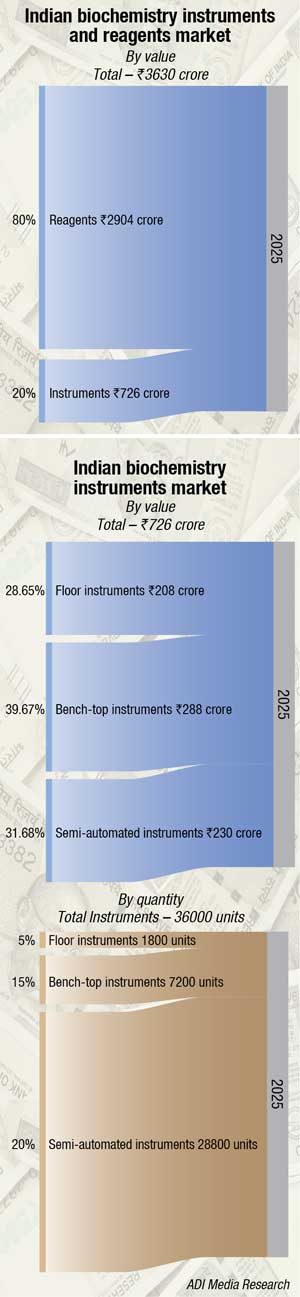

In 2025, the Indian biochemistry instruments and reagents market is estimated at around ₹3,630 crore, with reagents continuing to dominate and contributing nearly four fifths of total revenues. However, growth has become increasingly volume driven rather than value led, as large private hospital groups and national laboratory chains expand their networks and leverage centrally negotiated, high volume procurement contracts that intensify price competition across vendors.

|

Leading players – Indian biochemistry instruments and reagents market* |

|||

| Reagents | Fully automated instruments | Semi automated instruments | |

| Tier I | Transasia, and Agappe | Transasia and Mindray | Transasia |

| Tier II | Accurex and Roche; Beckman Coulter, Siemens, OCD, and Mindray | OCD, Agappe, Snibe, and Roche | Rapid Diagnostics and Mindray |

| Tier III | Biosystems, Fujifilm, Randox, URIT, Abbott, Rapid, AGD, CPC, Biogene, and regional brands | Sysmex, Biosystems, Fujifilm, Beckman, Abbott, Thermo Fisher Scientific, Siemens, and CPC | Agappe, Biosystems, Beacon, URIT, CPC, Dirui, Tulip, Microlab, and regional brands |

| Others | Trivitron, Tulip, Dirui, AGD, and Randox | ||

| Distributors e.g. Beacon for Bioelabs and Avantor for Mindray are not singled out in above table. | |||

| *Vendors are placed in different tiers on the basis of their sales contribution to the overall revenues of the Indian biochemistry instruments and reagents market.

ADI Media Research |

|||

The consolidation of purchasing into corporate procurement teams–at chains such as Apollo, Metropolis, and Thyrocare–has significantly reduced individual pathologists’ discretion in purchasing decisions. Instead, these groups now issue network wide RFPs covering dozens of sites, resulting in high instrument placements and sizeable reagent commitments but at compressed per test realizations and heightened expectations around service uptime, software upgrades, and automation support.

Government procurement in 2025 also showed healthy momentum, with strong order inflows from agencies such as TNMSC, KMSCL, OSMCL, and WBMSC. On the private front, large diagnostic and hospital networks continued expanding through new labs under the hub and spoke model, which has proven operationally effective. Key buyers included Redcliffe, PathCare Labs, Max Hospitals, KIMS, Mother Care (Kerala), Manipal TRUtest, Healthians, Orange Health Labs, CRL Diagnostics, and Indira IVF. Established players such as Metropolis, Dr Lal PathLabs, Agilus, and Thyrocare maintained steady procurement activity, while fresh RFPs for 2026 have already been floated by Apollo Hospitals, Metropolis, and Thyrocare, indicating ongoing demand momentum.

Despite seasonal concerns around vector borne outbreaks such as dengue and malaria, there was no pandemic like spike in test realizations, leaving the market growing in numbers, not in value. With price premiums difficult to defend, vendors are being pushed to differentiate through workflow automation, middleware or LIS integration, and advanced analytics or software solutions rather than through aggressive list pricing.

Within this environment, dry chemistry continues to represent a small but resilient niche–accounting for a high single digit share of the market–traditionally led by Ortho Clinical Diagnostics, followed by Fujifilm and newer domestic contenders such as Agappe. Meanwhile, wet chemistry and CLIA platforms maintain dominance across routine hospital and reference laboratory menus, supported by broader reagent portfolios and seamless integration with existing workflows.

Looking ahead to 2026, the market outlook points toward steady expansion of the installed base and rising test volumes, driven by new lab rollouts and the centralization of high end testing capabilities. However, instrument pricing and reagent margins are expected to remain under strain. Buyers are likely to favor multi site, multi year IVD contracts and show a stronger inclination toward software enabled, standardized CLIA systems that can be deployed uniformly across networks, rather than traditional premium priced, standalone biochemistry platforms sold on an account by account basis.

Smarter, faster, closer to patients – Biochemistry test is powering the next wave of diagnostics in India

Gaurav Bhide

Gaurav Bhide

Senior Product Manager-Biochemistry,

Transasia Bio-Medicals Ltd

Clinical biochemistry is redefining healthcare in India. Once concentrated in metro laboratories, it now shapes everyday clinical decisions across the country, supporting early detection, chronic disease monitoring, and critical care. Biochemistry accounts for nearly one-third of all diagnostic testing, growing at 8–10 percent annually, reflecting India’s rising demand for reliable, timely, and actionable insights. Over 60 percent of incremental diagnostic demand now comes from Tier-II, Tier-III, and rural areas. Compact, robust analyzers paired with long-lasting reagents bring standardized, high-quality testing to these regions, democratizing access to reliable diagnostics.

From imports to homegrown strength

Historically, Indian labs relied on imported analyzers and reagents, resulting in high costs and supply uncertainties. Today, localized instrument development and reagent production have cut cost per test by 20–35 percent, improved availability, and strengthened service support. Reagents alone account for 75–80 percent of total test costs, making domestic capabilities essential for affordable, high-quality diagnostics.

Automation that delivers impact

Automation is no longer optional–it is central to operational efficiency. Modern analyzers process 1,000–2,400 tests per hour with precision under 3 percent CV for core chemistries. This reduces analytical errors by 40–60 percent, accelerates turnaround times, and optimizes manpower, allowing laboratories to handle growing workloads while maintaining accuracy.

Driving care across therapy areas

Biochemistry informs care across India’s major health challenges. With over 100 million adults living with diabetes and millions at cardiovascular risk, panels such as glucose, HbA1c, lipids, electrolytes, and renal markers guide disease monitoring, therapy adjustments, and preventive strategies. Liver function tests and metabolic panels support management of NAFLD and chronic liver disease, while in critical care and oncology, frequent biochemical monitoring informs dosing, organ support, and therapy toxicity assessment. Each test provides actionable insights, enabling timely decisions and better patient outcomes.

Reagents as the backbone of value

Reagent-centric models are shaping the economics of biochemistry, aligning instrument utilization with long-term reagent quality and consistent results. This allows laboratories to focus on patient care while ensuring predictable costs and sustained performance.

In conclusion, biochemistry instruments and reagents are no longer just supporting laboratories, they are driving smarter, faster, and more accessible healthcare, setting the pace for the country’s next diagnostic breakthrough.

Global scenario

From a quantitative standpoint, multiple independent market studies converge on a picture of robust mid single digit annual growth through the end of this decade and into the early 2030s. Persistence Market Research, for example, estimates that the global biochemistry analyzer market will be around USD 4.4 billion in 2025 and is projected to rise to approximately USD 6.5 billion by 2032, representing a compound annual growth rate in the range of 5.5 to 6 percent. Comparable forecasts from other research houses place the 2030–2032 market size in the high single digit billions, with similar growth rates, underscoring that this is a resilient, structurally supported expansion rather than a short term spike. The growth is underpinned by a rising global volume of biochemical tests as clinicians lean more heavily on lab data to diagnose, stratify risk, and monitor increasingly complex chronic and acute conditions, embedding biochemical panels into routine and advanced care pathways alike.

At the clinical level, the proliferation of chronic, non communicable diseases forms the most visible demand driver for biochemistry analyzers and associated reagent systems. Diabetes, cardiovascular disease, dyslipidemia, chronic kidney disease, and cancer all require repeated, often lifelong biochemical assessment, covering parameters such as glucose, lipid profiles, renal and hepatic markers, electrolytes, and specific enzymes or proteins that track organ function and disease progression. As clinical practice guidelines across regions place growing emphasis on early detection, tight control of risk factors, and regular follow up, biochemical testing becomes a recurring element in routine care rather than an episodic investigative step reserved for acute clinical events. This shift is especially pronounced in aging populations, where multimorbidity is common and patients may undergo multiple panels per year across primary care, specialty clinics, and hospital settings, feeding a continuous stream of demand into laboratory workflows. The cumulative effect is a steady, compounding rise in test volumes that directly supports analyzer placement and reagent consumption over long time horizons and across different tiers of care.

The market is also shaped by structural changes in how laboratories are organized and operated as health systems consolidate and modernize. Across many high and middle income geographies, there is an ongoing consolidation of laboratory services into larger, more centralized facilities, whether within integrated hospital networks or commercial diagnostic chains spanning cities and regions. These larger entities have a strong incentive to invest in high throughput, fully automated biochemistry analyzers that can process thousands of samples per day, deliver consistent turnaround times, and integrate with broader automation lines that encompass pre analytical sorting, sample tracking, and post analytical validation and reporting. As a consequence, the fully automated analyzer segment has grown to dominate the market in both revenue and installed base, while semi automated systems, though still important in smaller or resource limited settings, gradually decline in relative share as technology costs fall and expectations around throughput and connectivity rise.

Technologically, biochemistry analyzers have undergone a profound evolution from manually intensive, stand alone instruments to highly integrated, software rich platforms that function as the nerve centers of clinical chemistry. Modern systems combine precise fluidics, temperature control, and photometric or electrochemical detection with sophisticated onboard software that orchestrates sample routing, reaction timing, calibration, and quality control in tightly controlled workflows. Many leading platforms now support multiple analytical modes, including endpoint, fixed time, and kinetic assays, within the same architecture, while offering flexible test menus that can be expanded or tailored according to laboratory needs and local epidemiology. This flexibility is particularly valuable as laboratories seek to consolidate multiple standalone instruments into fewer, more capable analyzers that reduce space requirements, simplify training, and streamline maintenance, while still covering a broad range of routine and specialized tests.

A key aspect of the market’s evolution is the shift from viewing analyzers purely as hardware to understanding them as nodes in a connected, data driven ecosystem where instruments, reagents, software, and services form an integrated whole. Connectivity to laboratory information systems and hospital information systems is now a basic expectation rather than a premium feature, enabling biochemistry analyzers to feed results directly into patient records and analytic pipelines. Through standardized communication protocols and middleware, biochemistry analyzers support automatic rule based validation, reflex testing algorithms, and autoverification of results where defined criteria are met, dramatically reducing manual data entry and the risk of transcription errors while accelerating the turnaround from sample receipt to actionable report. In larger networks, analyzers across multiple sites may be centrally monitored, with dashboards displaying throughput, quality control status, reagent levels, and instrument performance metrics in real time, giving technical and management teams unprecedented visibility into laboratory operations.

The rise of cloud based architectures has taken this connectivity logic a step further, extending the reach of the analyzer beyond the physical laboratory. Cloud connected analyzers allow remote diagnostics, software updates, and even predictive maintenance to be managed centrally, reducing downtime and travel costs for field service and enabling faster response to emerging issues. Surveys of clinical laboratories and vendor reports indicate that the share of facilities adopting cloud connected or IoT enabled analyzers has increased significantly in just a few years, reflecting growing comfort with remote management, centralized analytics, and the security frameworks that support them. For manufacturers, this connectivity layer opens new business models centered on service contracts, performance based agreements, and data driven advisory offerings, sitting alongside traditional hardware and reagent sales and changing the economics of analyzer deployment and lifecycle management.

From import dependence to indigenous strength – Localizing India’s biochemistry instruments and reagents

Bimal BK

Bimal BK

CEO,

Agappe Diagnostics Ltd

India’s clinical biochemistry instrument and reagents market is a vital subset of the overall in vitro diagnostics (IVD) and laboratory ecosystem. In 2023, the Indian biochemistry instruments and reagents market is driven by wider disease monitoring and expansion of diagnostic services.

Biochemistry analyzers/clinical chemistry analyzers are very important for tests like glucose profiles, lipid panels, liver and kidney function. They are part of a global biochemistry analyzer market valued at roughly USD 4.6 billion in 2024, expected to grow to nearly USD 7.9 billion by 2034. Regionally, the broader clinical chemistry analyzers segment reached around USD 142 million in India in 2023, with forecasts pointing to USD 210 million by 2030 indicating rising demand for automated and point-of-care solutions.

Despite robust demand, import dependence remains a key challenge. >60% of the IVD instruments/ reagents are imported including biochemistry analyzer components, reflecting a dominant import share in this category. Such reliance exposes clinical labs and hospitals to global supply fluctuations, foreign currency volatility, and cost pressures.

Addressing this, several Indian manufacturers are strengthening local capabilities. Companies like Agappe and others now produce fully automatic biochemistry analyzers, expanding availability beyond basic semi-automated devices and making technology more affordable for low to mid-sized labs.

Policy initiatives like Make in India and incentives for domestic medical device production are further pushing localization. These programs aim to reduce import penetration in instruments and reagents while strengthening regulatory support for indigenous innovation, calibration, and clinical validation processes.

Agappe stands as a key contributor to India’s growing clinical biochemistry ecosystem, backed by world-class manufacturing facilities that embody precision, reliability, and innovation. The company’s portfolio spans across a comprehensive range of semi-automated and fully automated clinical chemistry analyzers – from the Mispa Viva and Mispa Plus series to fully automated systems such as the Mispa Fab 120, Mispa CXL Pro Plus, and Mispa CX4, capable of delivering up to 400 tests per hour. By integrating advanced automation with robust reagent systems, Agappe continues to strengthen India’s self-reliance in diagnostic technology and support the expanding demand for accurate, efficient, and affordable biochemical testing solutions.

Regional pulse

Regionally, North America continues to account for the largest share of the global biochemistry analyzer market, supported by high per capita healthcare expenditure, advanced diagnostic infrastructure, and a well documented high prevalence of chronic diseases. The United States in particular hosts a dense network of hospital laboratories and commercial reference labs that rely heavily on high throughput, fully automated analyzers to support large testing volumes with stringent turnaround commitments and quality expectations. Reimbursement systems, while under increasing pressure to contain costs, still broadly support routine biochemical testing, and regulatory frameworks, though demanding, provide a clear pathway for the introduction of upgraded analyzer generations with enhanced connectivity, automation, and software features, including AI augmented capabilities where appropriately validated. Canada and parts of Latin America also contribute meaningfully to regional demand, especially where private diagnostic networks and public health laboratories are modernizing infrastructure and rolling out chronic disease management programs that rely heavily on chemistry panels.

Europe is likewise a mature, high value market for biochemistry analyzers, with strong adoption in Western and Northern European countries that operate universal or near universal health systems and maintain high standards for laboratory quality and accreditation. These systems place a premium on standardized diagnostics, evidence based protocols, and participation in external quality assessment programs, all of which favor analyzers with robust automation, reproducible performance, and comprehensive quality control and traceability capabilities. Procurement in several European jurisdictions increasingly incorporates sustainability and environmental criteria, which encourages the selection of analyzers designed for lower energy consumption, reduced water use, and greener reagent chemistries, aligning with broader green hospital agendas. In Central and Eastern Europe, growth is faster from a lower base as healthcare systems invest in modernizing hospitals and laboratories, often with EU structural funds or public–private partnerships, creating opportunities for both global vendors and regional players offering competitively priced solutions.

Asia Pacific is widely recognized as the fastest growing region in the biochemistry analyzer market and is expected to remain so over the forecast period. Large economies such as China and India, as well as rapidly developing Southeast Asian nations, are simultaneously expanding healthcare coverage, building new hospitals, and scaling up diagnostic capacity in urban and semi urban areas. This expansion is occurring against a backdrop of rising incidence of diabetes, cardiovascular disease, and cancer, often affecting younger populations and placing sustained strain on healthcare systems that are still building out infrastructure. Consequently, demand for accessible, reliable biochemical testing is surging, and laboratories are leapfrogging older generations of technology by adopting relatively modern, automated analyzers from the outset, often bundled with reagents and service agreements to de risk adoption. Government policies that encourage domestic manufacturing of diagnostic equipment and reagents, along with preferential procurement for locally produced or technology transfer enabled systems, further shape the competitive landscape, with local and regional manufacturers gaining share alongside established global brands.

Beyond the three primary regions, Latin America, the Middle East, and Africa constitute smaller but strategically important markets characterized by a mix of high end urban centers and vast underserved areas in need of basic diagnostic capability. In these regions, private diagnostic chains and large tertiary hospitals are key customers for advanced analyzers, while public health laboratories and smaller facilities may rely on mid range, semi automated, or refurbished systems that balance capability with affordability and simpler infrastructure requirements. Multilateral funding and international health initiatives can play an outsized role in enabling modernization projects that include biochemistry analyzers, particularly when focused on programs for HIV, tuberculosis, hepatitis, maternal health, or non communicable disease screening, where chemistry panels are core components of care algorithms.

Within the global market, segmentation by product and component reveals further nuance in value capture and competitive focus. Instruments themselves account for substantial upfront revenue, but over the lifecycle of an installed base, reagents and consumables often represent the majority of value, especially in high volume labs and networks. Most major manufacturers operate on a model in which analyzers are paired with proprietary reagent lines, calibrators, and quality control materials optimized for specific platforms, ensuring performance, regulatory compliance, and consistent quality, but also creating a lock in effect whereby laboratories commit to a given ecosystem for the duration of the analyzer’s usable life. As a result, competition for instrument placements is intense, with vendors often willing to offer favorable pricing, financing, or reagent rental arrangements for hardware in order to secure long term reagent revenue and deepen customer relationships.

Software and services represent another increasingly important layer of differentiation and value creation. Analyzer operating systems, user interfaces, and integration tools have become more sophisticated, supporting intuitive workflows, embedded troubleshooting guidance, and fine grained control over maintenance and QC routines that reduce operator burden and training time. Middleware that sits between analyzers and LIS/HIS systems adds rules engines, reflex testing algorithms, delta checks, and decision support, allowing laboratories to configure complex logic to govern which results are flagged, which are auto verified, and which trigger additional tests or alerts to clinicians, thereby standardizing post analytical processes. On top of this, vendors are beginning to integrate AI based analytics, especially for monitoring quality indicators, predicting instrument faults, or analyzing aggregate utilization patterns across networks of analyzers, further blurring the line between instrument supplier and digital performance partner.

Taking quality biochemistry testing beyond metros – Instruments and reagents for Bharat’s labs

Dr Rajesh Rengarajan

Dr Rajesh Rengarajan

Product Manger-Clinical chemistry reagents,

DiaSys Diagnostics India Pvt Ltd

India’s diagnostics sector continues to expand steadily, driven by a growing burden of chronic diseases, increasing preventive health awareness, and wider insurance penetration. At the core of this growth lies biochemistry testing–covering liver and kidney function tests, glucose, lipid profiles, proteins, and electrolytes–which forms the backbone of routine clinical decision-making. While metropolitan cities benefit from highly automated laboratories, ensuring consistent and reliable biochemistry testing beyond metros remains a key challenge and opportunity.

The diagnostics landscape outside large cities is highly fragmented. Most laboratories in tier-II, tier-III, and rural regions operate with limited space, manpower, and infrastructure, often relying on semi-automated or compact analyzers. These labs face practical constraints such as power fluctuations, variable sample loads, and the need for cost-effective operations. Dependence on imported instruments and reagents further adds to cost pressures, impacting test affordability for patients in non-metro regions.

To address these realities, both manufacturers and diagnostic providers are increasingly tailoring solutions for decentralized settings. Compact benchtop biochemistry analyzers with low water consumption, minimal maintenance requirements, and stable performance under variable conditions are gaining traction. Equally important is the availability of high-quality, stable reagents with longer shelf life and flexible pack sizes, allowing smaller labs to manage inventory efficiently without compromising accuracy.

Private diagnostic players are actively expanding their footprint beyond metros through hub-and-spoke models, satellite collection centers, and small-format laboratories. Improved logistics networks and better cold-chain management have made reagent supply more reliable, even in remote locations. Digital tools such as cloud-based laboratory information systems, remote troubleshooting, and automated quality checks are helping standardize reporting and improve turnaround times across dispersed networks.

Positive growth trajectory

The outlook for biochemistry testing beyond metros is strongly positive. Rising healthcare utilization in semi-urban and rural India, combined with growing trust in diagnostic testing, is driving volumes upward. Domestic manufacturing of instruments and reagents is improving affordability and reducing supply-chain dependence. Advances in automation, connectivity, and user-friendly design are making quality biochemistry testing viable in smaller laboratories. Together, these trends are enabling reliable, standardized diagnostics to reach across Bharat–bringing essential laboratory services closer to where patients live, work, and seek care.

From manual to fully automated labs

The core trend underpinning many of these developments is deeper automation across the biochemical testing chain as laboratories move from instrument centric operations toward end to end workflow design. Pre analytical automation, including sample sorting, barcoding, aliquoting, and transport via track systems, increasingly feeds directly into integrated analyzers or total lab automation lines, reducing manual handling and the associated risk of errors and contamination. Analytical modules spanning biochemistry, immunoassay, hematology, and coagulation are more frequently linked through common track infrastructures and software layers, enabling consolidated operations, balanced workloads, and unified control over multiple testing disciplines. Post analytical phases, from result validation to reporting, are streamlined with rules based middleware, autoverification, and electronic health record integration, cutting report release times and freeing up professional time for exception handling and complex interpretation rather than routine verification. This shift benefits biochemistry analyzers that can plug seamlessly into broader automation architectures, offer stable long run performance, and support standardized, scalable workflows; vendors that can demonstrate low downtime, predictable reagent consumption, and straightforward connectivity are gaining clear competitive advantage.

AI, machine learning, and smart connectivity

AI, machine learning, and smart connectivity are rapidly shifting from experimental add ons to foundational layers of the modern biochemistry analyzer ecosystem, reshaping how instruments are maintained, how quality is safeguarded, and how biochemical data is ultimately used in clinical decision making. In place of static, reactive workflows, laboratories are beginning to operate instruments that continuously learn from their own performance, from quality control data, and from the clinical context of the tests they run, allowing the analyzer environment to become progressively more predictive, adaptive, and tightly integrated with hospital information systems and data platforms. At the operational level, AI driven intelligence is transforming instrument uptime and service models by enabling machine learning based predictive maintenance that monitors telemetry such as sensor readings, error logs, reagent usage patterns, temperature profiles, and QC behaviors to detect subtle deviations that precede failures, flagging developing issues before they become critical and allowing service interventions to be planned with minimal disruption.

This predictive layer interacts closely with internal quality control, an area where AI and machine learning are beginning to show particularly strong impact in clinical chemistry. Conventional QC monitoring relies on established rules applied to control materials and manual or semi automated interpretation of Levey–Jennings plots, which can detect many types of shifts or trends but often only after they have fully manifested. Recent research demonstrates that machine learning models trained on historical QC data–incorporating analyte type, control level, reagent lot, instrument identity, operator, and temporal context–can identify patterns associated with impending IQC deviations well before they cross traditional rule thresholds, enabling preventive actions such as recalibration, reagent lot replacement, or targeted maintenance. As these QC and maintenance capabilities mature, they feed into the broader concept of quality 4.0 in clinical laboratories, where real time analytics, automation, and digital traceability converge to create continuously self monitoring systems that maintain analytical stability even under sustained high throughput conditions.

AI is also beginning to influence the clinical interpretation of biochemical data, often beyond the analyzer itself but tightly linked to its outputs. Early applications in clinical chemistry focus on predictive models that combine routine biochemical markers with other structured clinical variables, including vital signs, comorbidities, and demographic factors, to identify patients at high risk of deterioration or specific complications. Studies of AI based early warning systems in hospital wards and intensive care units show that algorithms using integrated lab and clinical data can outperform traditional scoring systems such as MEWS or SOFA for early detection of sepsis, cardiac events, and other adverse outcomes, improving predictive accuracy and contributing to reductions in mortality and unplanned ICU transfers. In these architectures, biochemistry analyzers function as core data generators, feeding timely lab results into real time risk engines that update patient risk scores as new data arrives across the episode of care, positioning chemistry data as a key input to predictive, personalized medicine.

Decentralization and point of care integration

Though core laboratories remain the mainstay of high throughput biochemistry, there is a noticeable push toward decentralization and point of care testing, especially for critical analytes such as electrolytes, cardiac markers, and lactate that inform urgent decisions. The automated analyzers market in general is seeing a rise in portable, compact, often battery operated systems that bring lab grade or near lab grade results closer to emergency rooms, ICUs, outpatient clinics, and even home care environments, aligning with broader shifts to distributed care models. For biochemistry analyzers, the trend toward decentralization and point of care deployment is reshaping how systems are designed, configured, and integrated into the broader diagnostic network, with compact analyzers being developed to run on minimal sample and reagent volumes while still delivering rapid, reliable readouts suitable for frontline decision making. In parallel, integration with digital tools has become essential for making these compact systems clinically useful rather than isolated devices, with many new analyzers supporting connectivity to smartphone applications, tablet interfaces, or web based dashboards that present results in clinically meaningful formats, linked to patient identifiers and historical data and feeding validated results into electronic health records or centralized systems in near real time.

Evolving role of clinical biochemistry in modern healthcare

Pramod Sharma

Pramod Sharma

Business Development Manager,

BioSystems Diagnostics

Modern healthcare relies fundamentally on clinical biochemistry for disease diagnosis, monitoring, and therapeutic decision-making. Despite its central role, the discipline faces several operational challenges, including sampling inefficiencies, limitations in analytical precision, and scalability constraints. However, significant advances in laboratory instrumentation and analytical technologies have markedly increased the sophistication of clinical laboratories. These innovations have enabled the consolidation of a wide range of assays into the core clinical chemistry laboratory, including tests for tumour markers, therapeutic drug monitoring, endocrinology, reproductive health, and drugs of abuse.

Clinical chemistry is still one of the biggest IVD segments in India – It is estimated that clinical chemistry at ~24.8 percent of IVD revenue share, is among the largest segments in India, the market is expected to generate approximately USD 480 million in revenue by 2030. India is part of the fastest-growing Asia-Pacific region for clinical chemistry analyzers. This growth is driven by Disease Burden: Increasing prevalence of lifestyle diseases, diabetes, and cardiovascular issues boosts demand for tests like lipid and metabolic panels. Healthcare infrastructure–growing investments in healthcare infrastructure and government programs (like Ayushman Bharat) expand access to diagnostics. Preventive care–rising awareness about routine check-ups fuels demand for basic metabolic and electrolyte panels.

Key trends shaping the clinical chemistry market

- Automation-first labs (TLA, tracks, pre/post analytics).

- Decentralized chemistry (compact analyzers, dry chemistry, near-patient use).

- Connectivity plus fleet management (middleware, QC analytics, remote service).

- Menu expansion and better specificity (select LC-MS/MS migration, improved assays).

- Cost-performance engineering for emerging markets (robustness, low water, heat tolerance, serviceability).

BioSystems committed to providing robust and reliable analyzers and reagents in Clinical Chemistry segment supported by a world-class manufacturing facility that meets the highest quality standards. Through stringent quality system, advance technologies and dedicated service support, ensuring consistent performance and long-term customer satisfaction.

BioSystems continues to position itself as one of the most trusted service providers in clinical chemistry segment. This holistic approach not only drives sustainable growth but also reinforces our commitment to delivering value, reliability and confidence – today and into the future.

Sustainability and green lab imperatives

Sustainability is emerging as a strategic differentiator in the analyzer market as clinical laboratories face increasing pressure to reduce their environmental footprint from chemical waste, energy use, and consumables. Biochemistry analyzers contribute to all three elements through reagents, disposable consumables such as cuvettes and pipette tips, and energy intensive operation, particularly in large, continuously operating laboratories. Manufacturers of biochemistry analyzers are responding by designing instruments with lower energy consumption, more efficient water usage, and sleep or idle modes that reduce power draw during off peak times, as well as by developing reagent formulations that minimize hazardous solvents and reduce packaging waste, aligning with green chemistry principles such as safer solvents, waste prevention, and design for energy efficiency. Offering take back or recycling programs for consumables and instrument components is also becoming more common as part of broader corporate sustainability commitments that resonate with health systems adopting environmental criteria in procurement.

Despite its positive momentum, the biochemistry analyzer market faces several structural challenges that stakeholders must navigate. High capital costs and total cost of ownership remain barriers for smaller laboratories and facilities in low resource settings, even when the clinical benefits of automation and modern analyzers are clear. Proprietary reagent models can limit price flexibility, and economic shocks or currency fluctuations can further strain budgets, particularly where public procurement dominates and foreign exchange volatility affects imported systems and consumables. Workforce constraints also remain acute, as many regions report shortages of trained laboratory professionals capable of managing complex analyzers, interpreting QC trends, and ensuring compliance with accreditation standards, which can hamper optimal utilization of advanced platforms. Regulatory and reimbursement landscapes add another layer of complexity, especially when new biomarkers, specialized panels, or advanced software features outpace existing coding, coverage, and payment structures, dampening incentives to invest in top tier systems where revenue capture is uncertain. Interoperability and data security concerns accompany the spread of connected and cloud linked analyzers, requiring continuous investment in secure software architectures, encryption, and access controls to safeguard patient data while enabling the benefits of digital integration.

Looking ahead, the outlook for the biochemistry analyzer market is one of continued, measured expansion and deepening strategic relevance within healthcare systems worldwide as diagnostics becomes even more central to care delivery and health system performance. Demand for biochemical testing is unlikely to plateau in the foreseeable future, given persistent chronic disease burdens, the spread of preventive and screening programs, and the integration of lab data into predictive and personalized medicine frameworks that depend on robust, high quality chemistry data. Technology trends are pushing analyzers toward greater automation, smarter connectivity, and tighter integration with multidisciplinary diagnostic platforms that combine chemistry, immunoassay, hematology, and molecular testing within unified, highly automated workflows, while environmental and resource considerations are prompting a rethinking of how instruments and reagents are designed, deployed, and supported over their lifecycle. For manufacturers, success will depend on the ability to deliver not just reliable analyzers and high quality reagents, but holistic solutions that encompass software, services, training, and sustainability, tailored to the specific needs of different regions and tiers of the healthcare system. For laboratories and health systems, the challenge lies in choosing platforms that can scale with rising demand, integrate smoothly into evolving digital architectures, and support both central and decentralized testing models, while remaining financially and environmentally sustainable over the long term. Within this dynamic landscape, biochemistry analyzers will remain a cornerstone technology, providing the biochemical insights that underpin diagnosis, monitoring, and increasingly prediction across virtually every domain of modern medicine, and forming a critical interface where reagents, analyzers, and intelligence converge to redefine the future of laboratory diagnostics.