Reports

Healthcare industry overview

India’s healthcare market is set to quadruple by 2026, driven by innovation, investment, and policy reforms, according to a Dolat Finserve presentation.

The Indian healthcare market is poised for exceptionally rapid expansion over 2023–2032, with total market size projected to rise from approximately ₹17.62 trillion in 2020 to ₹81.30 trillion by 2026, representing a compound annual growth rate of nearly 29.8 percent during 2021–2026.

According to Dolat Finserv Private Limited (Investment Banking Division), this analysis positions healthcare as one of India’s fastest-growing industries, driven by rising demand for quality care, demographic shifts, and a policy push for greater coverage and infrastructure. Within this topline, hospitals, digital health, diagnostics, pharmaceuticals, medical devices, insurance, and medical tourism together form a diversified but tightly interconnected growth engine.

Market size, trajectory, and structure

India’s healthcare market was valued at approximately ₹17.62 trillion in 2020 and is expected to more than quadruple to ₹81.30 trillion by 2026. This trajectory implies that healthcare will grow far faster than overall GDP, increasing its share in national output and signalling sustained opportunities for investors, operators, and technology providers. The analysis attributes this surge to rising non-communicable disease burden, increasing health awareness, urbanisation, and growth in both public and private health insurance, which together expand the paying patient base and push more care into formal systems.

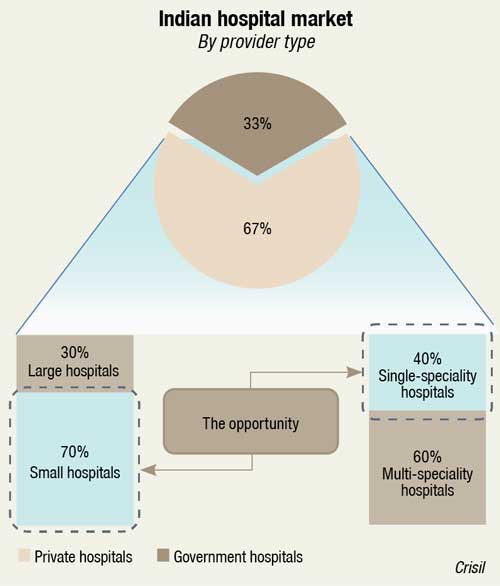

The report disaggregates the market into nine major segments: hospitals, outpatient care centres, pharmaceuticals, medical equipment and supplies, diagnostic services, digital healthcare, research and development, medical insurance, and medical tourism. In 2020, hospitals alone accounted for around 32 percent of total healthcare revenue, underscoring their central role as the primary driver of revenue and employment. However, growth is not evenly distributed: digital healthcare, diagnostics, and medical devices are expected to clock above average CAGRs as technology adoption accelerates, preventive care gains traction, and more services shift toward home and ambulatory settings.

Outlook-2026

Several structural growth drivers underpin the outlook to 2026. The report highlights a sharp increase in demand for home-based healthcare devices and digital health solutions after the pandemic, with teleconsultations, remote monitoring, and app-based care platforms now embedded in routine practice rather than being temporary stopgaps. Liberalised foreign direct investment norms and a sharper government focus on health–through insurance schemes, infrastructure programmes, and higher budgetary allocations–have improved the investment climate and catalysed capacity expansion in hospitals, diagnostics, and manufacturing. International agencies and trade bodies also point to India’s growing role as a medical tourism and med tech hub, further reinforcing the positive medium-term scenario.

At the same time, it stresses that India continues to face significant gaps in physical infrastructure, workforce, and financial protection that could moderate the speed at which this potential is realised. Shortages of hospital beds, doctors, nurses, and allied professionals, especially outside major cities, combine with uneven health insurance penetration to limit access and strain quality, even as aggregate spending surges. These constraints, however, are presented less as structural ceilings and more as indicators of the addressable space: they define where capital and policy need to focus between 2023 and 2032, and they are central to why the market can still sustain a near 30 percent CAGR to 2026 and strong growth beyond.