Cath Labs

Cath labs – Where capital meets cardiac care

Where intervention meets institutional advantage, growth begins.

India’s cardiac care ecosystem stands at a critical inflection point. Surging incidences of coronary artery disease (CAD), ST-elevation myocardial infarction (STEMI), structural heart disorders, and arrhythmias are driving urgent demand for interventional care. Lifestyle shifts, rising diabetes and hypertension prevalence, an ageing population, and persistent late-stage diagnoses are rapidly expanding the patient pool across urban and semi-urban markets. Demand now extends well beyond routine cardiology consultations, accelerating toward advanced diagnostics, angioplasty, electrophysiology, valve interventions, and minimally invasive procedures–all of which depend on high-quality catheterisation laboratory infrastructure.

Gone are the days when cath labs were prestige assets confined to flagship hospitals. Today, they are the operational backbone of tertiary and quaternary care, attracting elite specialists, enabling complex emergency responses, improving clinical outcomes, and generating high-acuity revenue. For multi-specialty hospitals, a top-tier cath lab signals readiness for complex cardiac interventions, stroke-related vascular procedures, and round-the-clock emergency capability. Facilities without this edge increasingly lose both patients and physicians to better-equipped competitors.

The next major demand wave is building in Tier-II and Tier-III cities, where rising household incomes, expanding insurance coverage, growing health awareness, and strengthening referral networks are transforming patient behaviour. Residents no longer accept the burden of long-distance travel for urgent angioplasty or arrhythmia management when quality care is available closer to home. This shift is creating a compelling case for decentralised cardiac hubs, particularly in high-disease-burden districts where specialist supply has not kept pace with demand.

Meanwhile, India’s ongoing hospital expansion is generating a significant capital expenditure wave. As providers add beds, develop new campuses, and strengthen clinical capabilities, cath labs are rising to the top of investment priority lists–not as discretionary luxuries, but as essential revenue-generating assets. They drive occupancy rates, lift average revenue per occupied bed, and generate cross-referrals across ICU, imaging, surgery, and rehabilitation services. Cath labs have decisively evolved from showpieces to strategic growth accelerators.

Indian market dynamics

Government procurement policy is reshaping competitive dynamics in the Indian cath lab market. With public tenders restricted to domestically manufactured products through GeM and HLL Lifecare, multinational corporations are accelerating their Make in India investments – GE HealthCare led this shift in 2023, followed by Siemens Healthineers in 2026.

A significant clinical shift is also underway–cath labs are increasingly used for modalities beyond cardiology, expanding the addressable market and creating new therapy opportunities. Small-detector systems are gaining relevance in this context, while large-detector platforms – predominantly procured by the Government of India and large corporate hospital chains – serve interventional radiology, oncology, and pulmonology. The neurology segment, however, remains the single largest growth driver, led by stroke management and neurovascular angiography.

|

Leading players* 2025 |

|

| Imported | |

| Tier I | Philips |

| Tier II | GE & Siemens |

| Others | Canon and Shimadzu |

| Recent entrants | United Imaging and Neusoft |

| Indigenous brands | |

| Tier I | Innvolution |

| Tier II | Allengers and GE |

| Tier III | Skanray |

|

*Vendors are placed in different tiers on the basis of their sales contribution to the overall revenues of the Indian cath labs market. ADI Media Research |

|

Chinese players such as United Imaging and Neusoft have entered the Indian market, though the industry remains cautious about sourcing from countries that share a land border with India, given concerns about data privacy and national security. Canon secured a notable government order for 13 systems across two batches – 6 units in 2025 and 7 in 2026 – for new AIIMS facilities, including one for AIIMS Delhi.

Why India’s cath lab economics need a manufacturing answer, not an import one

RS Kanwar

RS Kanwar

Managing Director,

Allengers Medical Systems Limited

Rising demand for affordable cardiac care

India’s healthcare landscape is rapidly evolving, with increasing demand for advanced cardiac care and interventional procedures. However, the economics of cath labs in India continue to be heavily influenced by imported systems, resulting in high acquisition cost, expensive maintenance, dependency on foreign spare parts, and long service turnaround time. For a country aiming to strengthen affordable healthcare delivery, the answer lies not in imports, but in empowering indigenous manufacturing.

The need for indigenous manufacturing

The Make in India vision has already demonstrated how local manufacturers can transform industries through cost optimization, innovation, and self-reliance. The cath lab segment is no exception. India requires advanced yet economically viable imaging solutions tailored to the Indian healthcare infrastructure and patient volumes.

Domestic manufacturers today can deliver world-class cath lab, x-ray, C-arm, and mammography systems that meet international quality and regulatory standards while significantly reducing overall costs. Beyond affordability, indigenous manufacturing offers faster installation support, readily available spare parts, localized service networks, and customized solutions tailored to Indian diagnostic centers.

Reducing dependency on imports

Import dependency not only increases financial burden but also exposes healthcare institutions to currency fluctuations, supply chain disruptions, and delayed upgrades. In contrast, Indian manufacturers offer agility, ongoing technical support, and the ability to innovate to meet local clinical requirements.

Strengthening India’s healthcare future

Additionally, supporting Indian manufacturing directly contributes to employment generation, skill development, technological advancement, and export growth. India is steadily emerging as a global hub for medical device manufacturing, with Indian-made systems now being exported to several countries worldwide.

As India advances toward healthcare self-reliance, a clear distinction between Made in India and Assembled in India becomes essential. Well-defined Indian content standards will not only safeguard genuine manufacturers but also accelerate indigenous innovation, technological excellence, and long-term national competitiveness in the medical device sector.

For hospitals and healthcare providers, the true value of an offer lies in agility, ongoing technical support, and the ability to innovate to meet local needs not only in procurement costs but also in lifecycle economics, uptime reliability, service accessibility, and long-term sustainability. A manufacturing-driven approach ensures that advanced cardiac care becomes more accessible, affordable, and scalable across India.

Despite rising prices over the past two to three years – driven in part by the depreciation of the Indian rupee – users consistently prefer premium systems that support multiple modalities beyond cardiology. Biplane systems, retailing at an average unit price of ₹9 crore, are primarily procured by the government and large corporate chains, with neurology accounting for the majority. In oncology, TACE and TARE procedures are increasingly performed in these suites. Tier-II and Tier-III cities are the primary growth engine, with domestically manufactured systems finding strong uptake due to competitive pricing.

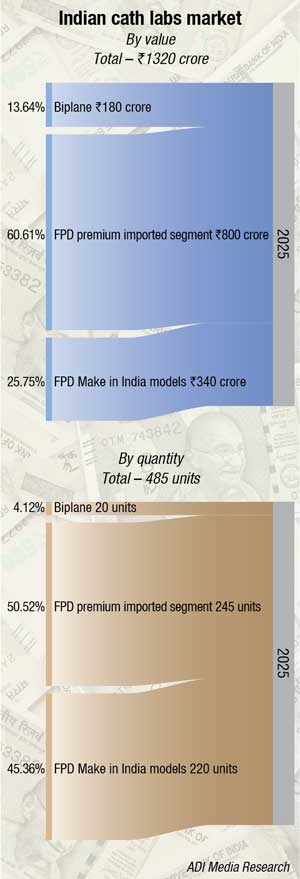

Market size and epidemiological backdrop. The Indian cath lab equipment market is estimated at ₹1,320 crore in 2025, with unit volumes approaching 485 systems. India’s broader cardiovascular devices market is projected to reach Rs 36000 crore by 2033 – nearly double current levels – reflecting both rising demand and a decisive shift toward advanced, technology-enabled cardiac care spanning interventional cardiology, cardiac rhythm management, and cardiovascular surgery. The cath lab equipment segment sits at the center of this transformation, serving as the physical infrastructure through which the vast majority of coronary interventions, structural heart procedures, electrophysiology, and neurovascular cases are delivered.

Cardiovascular disease is the leading cause of death in India, accounting for nearly one in four fatalities, with prevalence rates expected to rise further. Coronary artery disease affects 2.5 percent–12.6 percent of urban populations and 1.4 percent–4.6 percent of rural populations, reflecting pronounced geographic and socioeconomic disparities. India’s cath lab density currently stands at just 1.5–1.75 per million people – compared to 5–10 per million in developed markets – underscoring the structural deficit that sustains long-term procurement demand.

Segment dynamics. The trend toward higher-capability systems has deepened through 2025–2026. Premium imported flat-panel detector (FPD) systems continue to dominate in value, accounting for 60 percent of the total market, with support from large private hospital chains. Biplane systems are steadily gaining share–their clinical versatility – simultaneously supporting cardiac, neuro, vascular, and pediatric/congenital indications from a single installation – makes the investment case compelling for multi-specialty hospitals and new greenfield cardiac centers. The indigenous FPD segment faces continued margin pressure, as domestic manufacturers remain dependent on imported components despite retaining a pricing advantage in government tenders.

AI and intravascular imaging. The 15th India Live Cardiology Conference, held in March 2026 at Bharat Mandapam, New Delhi, crystallized the direction of clinical adoption. The conference highlighted a critical transition from traditional angiography toward AI-augmented intravascular imaging. AI-powered tools integrated with OCT and IVUS can now automatically detect calcium deposits, map vessel architecture, evaluate stent placement, classify plaque morphology, and recommend optimal stent sizing – with accuracy exceeding manual interpretation alone. AI has evolved from a post-procedural analysis tool to a real-time decision-making co-pilot in the catheterization lab. Indian tertiary centers and high-volume facilities are beginning to adopt these capabilities, with intravascular imaging guidance increasingly specified in RFPs from leading private hospital chains.

Structural heart and TAVR. TAVR offers significantly faster recovery – 2–3 days versus 7–10 days for open surgery – with quality-of-life outcomes comparable to surgical intervention and at substantially lower cost than global markets. Each structural heart case requires a high-specification cath lab suite, ideally biplane or hybrid, with advanced 3D fluoroscopic capability and real-time intracardiac echocardiography integration, making TAVR growth a direct driver of premium system procurement.

Electrophysiology – The fastest-growing sub-segment. Electrophysiology procedures for arrhythmia management are driving procedural demand at a rate that outpaces growth in coronary interventions. The rising incidence of atrial fibrillation – driven by India’s aging and increasingly sedentary population, combined with improving referral pathways – is filling EP lab schedules at tertiary hospitals and specialty cardiac centers. Dedicated EP systems and 3D mapping platforms are increasingly co-specified alongside angiography systems in new cath lab builds.

Robotic-assisted PCI. The commercial launch of robotic-assisted PCI systems – including Robocath’s R-One, currently the only commercially available robotic PCI platform – has validated a disruptive approach to precision catheter-based therapy. A small number of leading Indian cardiac centers, primarily in metropolitan areas, are evaluating or piloting robotic PCI. While volumes remain nascent, these early reference sites are seeding a technology pathway that will influence cath lab design and procurement decisions at flagship institutions over the coming years.

Government procurement and access inequity. India’s National Health Mission has funded the expansion of cath labs in district hospitals, with Maharashtra and Tamil Nadu among the leading states in establishing new cardiac units. However, rural populations continue to face shortages of cardiologists, inadequate infrastructure, long travel distances, and treatment delays. Government tenders in this segment typically favor lower-cost FPD systems or indigenously assembled platforms due to strict price sensitivity, creating a structurally bifurcated market in which procurement criteria and product specifications differ markedly between public and private channels.

Multi-specialty utilization. The business case for high-end, large-detector cath lab systems rests substantially on the ability to generate revenue across multiple clinical specialties – cardiology, peripheral vascular, neurology, oncology, and orthopedics – from a single suite. Large-format flat-panel detectors enable whole-body coverage in a single acquisition run, reducing patient repositioning and supporting growing volumes of complex oncological and peripheral vascular procedures alongside cardiac cases. Hospitals in Tier-I and larger Tier-II cities are increasingly designing cath labs with explicit multi-specialty utilization in their financial models, directly driving biplane demand and premium system adoption.

Structural constraints

Cardiology training in India comprises three years of internal medicine followed by three years of cardiology, with a limited number of accredited fellowships concentrated in interventional cardiology, electrophysiology, and pediatric cardiology. Structured programs in heart failure, transplantation, adult congenital heart disease, and structural interventions are largely absent; many complex procedures are performed by general cardiologists or through non-accredited fellowships with variable oversight. This human resource gap constrains the full utilization of sophisticated cath lab systems post-procurement and limits the pace at which new centers outside major cities can be operationalized effectively. High capital costs – mid-range systems cost ₹2.5 to ₹3.75 crore per unit alone, with total commissioned costs often higher – further restrict access for smaller hospitals and cooperatives, even where clinical demand exists.

Global scenario

The global cath lab market is entering a stronger growth cycle, driven by the convergence of cardiovascular disease burden, demographic ageing, rising diabetes and obesity rates, and growing demand for faster, safer interventional therapies. The market was valued at USD 4.14 billion in 2024 and is projected to reach USD 4.36 billion in 2025, expanding to USD 7.43 billion by 2035 at a compound annual growth rate (CAGR) of 5.46 percent, according to Market Research Future. This trajectory reflects sustained investment in cath lab infrastructure not only for angioplasty, but also for electrophysiology, structural heart procedures, peripheral vascular interventions, stroke thrombectomy, and minimally invasive therapies that reduce patient recovery time and improve long-term outcomes.

Technological advancement remains a primary growth engine. Advanced fluoroscopy, 3D imaging, AI-assisted workflow tools, intravascular ultrasound (IVUS), optical coherence tomography (OCT), fractional flow reserve (FFR) measurement, and remote clinical support systems are transforming cath labs into smarter, more efficient procedural platforms. Rising insurance penetration, expanding private hospital chains, and the migration of procedures into ambulatory surgical centres are further widening market opportunities. Governments across emerging economies are simultaneously supporting healthcare infrastructure expansion through cardiac care access programs, broader insurance coverage, public-private partnerships, and domestic medical device manufacturing incentives–all of which strengthen the potential for cath lab deployment.

The market also faces meaningful headwinds that can constrain growth momentum. High capital expenditure for installation, expensive recurring consumables–including catheters, guidewires, balloons, and contrast media–and rising annual maintenance costs remain significant barriers, particularly for mid-sized hospitals and low-income geographies. Shortages of trained interventional cardiologists, cath lab nurses, radiographers, and biomedical engineers limit capacity expansion. Regulatory approval timelines, reimbursement uncertainty, import dependence, tariff volatility, and supply chain disruptions can delay procurement decisions. In many developing markets, affordability pressures and weak referral networks continue to suppress utilisation despite a growing disease burden.

North America remains the largest cath lab market globally, supported by mature healthcare systems, strong reimbursement frameworks, high procedural volumes, rapid technology adoption, and the presence of leading OEMs. The United States continues to set the pace in structural heart therapies, electrophysiology, outpatient procedure migration, and AI-enabled imaging. Hospitals there are increasingly focused on productivity optimisation, radiation reduction, software integration, and lifecycle asset management.

Asia-Pacific is the fastest-growing region and presents the most significant long-term expansion opportunity. China and India are primary growth drivers, fuelled by hospital construction, rapid urbanisation, rising middle-class healthcare spending, increasing cardiovascular disease awareness, and government-backed modernisation programs. Tier-II and Tier-III cities are emerging as high-priority growth markets where access gaps remain substantial. Cost-effective systems, refurbished labs, hub-and-spoke delivery models, and public-private partnerships are expected to accelerate market penetration. Japan, South Korea, and Southeast Asian markets are also upgrading cath lab capabilities to address ageing populations and growing complex cardiac caseloads.

Competitive intensity is rising as the market transitions from hardware-centric competition to platform competition. Established OEMs continue to leverage core strengths in imaging quality, reliability, hybrid lab capability, and service reach. Meanwhile, newer entrants are gaining ground by offering AI-driven analytics, workflow software, modular upgrade pathways, and faster deployment timelines. Procurement teams now evaluate interoperability, cybersecurity, digital reporting, predictive maintenance, and scalability alongside image quality metrics. The future winners will likely be companies with the strongest integrated ecosystems and most credible technology roadmaps–not simply the best machine available today.

Strategic partnerships and acquisitions are accelerating this convergence. Device manufacturers are aligning with software firms, telehealth providers, cloud analytics companies, and hospital networks to deliver integrated cath lab solutions. These alliances are improving innovation velocity, widening geographic reach, reducing service downtime, enhancing clinician training, and creating bundled offerings that simplify hospital adoption decisions.

Volumes fall, value rises

Demand patterns inside cardiac catheterisation laboratories are undergoing a fundamental shift. Globally, routine diagnostic angiography is declining as non-invasive imaging modalities–coronary CT angiography, cardiac MRI, stress imaging, and AI-driven risk stratification tools–accurately identify patients who genuinely require invasive investigation. Diagnostic catheterisation, once the default pathway for suspected coronary disease, is increasingly reserved for cases where non-invasive findings are inconclusive or intervention is immediately anticipated. This realignment reflects the principles of precision medicine–lower procedural risk, reduced unnecessary exposure, and more efficient use of constrained cath lab capacity.

Interventional volumes, however, are expanding strongly. Percutaneous coronary intervention (PCI), electrophysiology procedures, peripheral vascular interventions, and a rapidly growing structural heart portfolio–including transcatheter aortic valve replacement (TAVR), transcatheter edge-to-edge repair (TEER), left atrial appendage closure, and emerging tricuspid and mitral valve therapies–are collectively driving a more complex and more valuable case mix. Even congenital heart disease correction is migrating toward catheter-based approaches, reducing reliance on open cardiac surgery and requiring highly specialised laboratory capabilities.

Structural heart procedures are particularly redefining what it means to operate a high-performing cath lab. These cases demand advanced clinical expertise, premium imaging infrastructure, multidisciplinary team coordination, anaesthesia support, extended room time, and specialised devices. They generate a fundamentally different financial and operational profile compared to routine diagnostic work. For tertiary referral hospitals, a functioning structural heart program anchors brand positioning, attracts subspecialty cardiologists, drives complex referrals, and future-proofs the cardiovascular service line.

This shift in the composition of demand effectively retires the volume-only performance framework. High-throughput diagnostic processing is no longer the primary value driver. What matters today is procedural complexity management, clinical outcome consistency, per-case contribution margin, and efficient room utilisation. Hospitals must reconfigure scheduling protocols, staffing models, physician engagement strategies, inventory management, and reimbursement approaches to compete effectively in this environment. The cath lab of tomorrow is not a diagnostic processing unit–it is a high-complexity cardiovascular intervention platform.

ROI beyond angiography

The financial case for cath lab investment requires a fundamentally broader analytical lens. Traditional performance metrics–diagnostic catheterisation volumes, angioplasty case counts, or room occupancy rates–no longer capture true economic value. As cardiac care complexity increases and non-invasive imaging reduces unnecessary angiograms, the real return on a high-performing cath lab is distributed across the entire hospital system, not confined to the procedure room alone.

A strategically positioned cath lab anchors emergency cardiovascular care and secures high-value patient volumes that would otherwise migrate to competitor facilities. In acute myocardial infarction scenarios, rapid on-site intervention dramatically improves clinical outcomes, drives emergency admissions, and establishes the hospital as the regional cardiac emergency destination. Beyond acute care, a strong cath lab generates sustained referral flows from general practitioners, diabetologists, internists, and satellite clinics seeking a credible advanced cardiac partner. The result is a continuous patient pipeline feeding outpatient, inpatient, and ICU service lines.

Downstream revenue contribution is equally significant. Cath lab patients consistently generate ancillary utilisation across ICU stays, step-down care, diagnostic imaging, pathology, pharmacy, cardiac rehabilitation, and long-term disease management. Complex interventional cases frequently transition into surgical handoffs, electrophysiology procedures, vascular interventions, or chronic cardiology follow-up programmes. Viewed through a cardiovascular service-line framework, the cath lab functions as a revenue multiplier–generating economic activity across multiple hospital departments simultaneously.

Operational efficiency directly determines financial performance. Faster room turnaround times, optimised case scheduling, and a deliberate focus on high-acuity procedures–PCI, structural heart interventions, complex electrophysiology–significantly improve EBITDA per lab hour. In many institutions, a smaller volume of complex, high-margin cases delivers superior financial performance compared to high throughput of lower-acuity diagnostic procedures. This is why investments in staffing optimisation, workflow redesign, intelligent supply management, and technology upgrades translate directly to improved cath lab financial contribution.

The reputational return should not be underestimated. A high-performing cath lab signals advanced clinical capability, 24/7 emergency readiness, and institutional commitment to comprehensive cardiac care. It attracts top-tier interventional cardiologists, cardiac intensivists, surgeons, and referring physicians who seek well-equipped environments. Patients increasingly select hospitals with strong cath lab infrastructure for both emergency care and planned interventional procedures. Together, these factors make cath lab ROI today significantly broader, deeper, and more strategically important than traditional capital expenditure accounting models suggest.

Buy smart, scale fast

Cath lab procurement has evolved from a straightforward capital expenditure decision into a multidimensional strategic choice that shapes clinical capabilities, financial margins, and market positioning for years to come. Greenfield hospitals and flagship tertiary centres frequently opt for new-generation premium systems to launch with best-in-class imaging, AI-enabled workflow tools, reduced radiation dose profiles, and upgrade-ready platforms. For these facilities, the cath lab is simultaneously a clinical capability statement and a powerful referral magnet.

For many mid-sized hospitals, however, a more financially disciplined route involves upgrading existing installations rather than full system replacement. Flat-panel detector retrofits, software enhancements, table modernisation, and workflow automation tools can meaningfully extend asset life while improving image quality and procedural throughput at a substantially lower cost than complete system replacement. This approach enables hospitals to remain competitive without disrupting ongoing operations or overextending capital budgets.

Refurbished cath lab systems are gaining serious strategic traction in cost-sensitive markets, Tier-II and Tier-III cities, and standalone cardiac centres. Properly recertified and reconditioned systems can deliver reliable clinical performance at significantly lower entry costs, enabling providers to launch services faster and improve return-on-investment timelines. For many operators, refurbished equipment is no longer a compromise–it is a deliberate and commercially sound market entry strategy.

The central procurement question has shifted decisively away from purchase price alone. Leading decision-makers now evaluate total lifecycle value–annual maintenance obligations, uptime reliability, spare-part availability, detector generation, software compatibility, energy efficiency, and upgrade pathway clarity. In the current environment, the winning procurement strategy prioritises lifecycle value optimisation over short-term cost minimisation.

The Tier-II gold rush

India’s next major cath lab growth story is unfolding outside its metropolitan centres. Across many districts, patients still lack reliable access to angioplasty-ready facilities, forcing critically ill cardiac patients to travel long distances for time-sensitive interventions. In acute myocardial infarction, these delays carry severe consequences–additional myocardial damage, prolonged recovery, elevated mortality risk, and significantly higher downstream treatment costs.

This access gap represents one of the most significant white-space opportunities in Indian healthcare. As cardiovascular disease awareness rises, insurance penetration expands, and non-communicable disease burden grows, demand for advanced cardiac services is accelerating well beyond metropolitan boundaries. Patients are increasingly choosing high-quality treatment closer to home rather than the financial and logistical burden of traveling to large urban hospitals.

For regional hospital chains and ambitious standalone providers, cath labs can function as powerful anchor assets in these markets. A functioning cath lab drives interventional cardiology volumes while simultaneously attracting referrals for ICU care, diagnostic imaging, surgery, pharmacy, rehabilitation, and chronic disease management. It transforms a general care centre into a credible tertiary destination capable of retaining complex patients within the regional healthcare ecosystem.

Innovative delivery models will be essential to unlocking this market at scale. Mobile cath labs, hub-and-spoke referral networks, shared-capacity arrangements, and recertified refurbished systems can enable providers to enter underserved geographies with reduced capital risk and faster deployment timelines. The next chapter of cath lab expansion in India will be written in Tier-II and emerging regional markets–where access gaps are largest, growth potential is strongest, and first-mover advantages are most durable.

The rise of hybrid labs

Hybrid cath labs are rapidly becoming the defining battleground for advanced cardiovascular care–integrating the precision imaging capability of an interventional suite with the sterility, space, and surgical infrastructure of a full operating theatre. As demand grows for minimally invasive yet high-risk procedures, hospitals are investing in purpose-built environments that can transition seamlessly between catheter-based intervention and open surgery within minutes. These spaces are increasingly indispensable for TAVR, complex endovascular repair, congenital heart disease interventions, and high-acuity structural heart procedures that require real-time multidisciplinary collaboration.

For premium hospital groups, a hybrid lab is more than infrastructure–it is a clear signal of clinical ambition and institutional commitment to comprehensive, high-acuity cardiovascular care. It helps attract leading interventional cardiologists, cardiac surgeons, anaesthesiologists, and the complex referral volumes they bring. While capital costs are substantially higher than standard cath lab installations, the financial payoff comes through a superior case mix, stronger revenue realisation per procedure, better clinical outcomes, and enhanced institutional brand positioning. For hospitals targeting movement up the acuity ladder, hybrid cath labs are fast becoming a logical and necessary strategic investment.

Radiation safety as a boardroom KPI

Radiation safety has moved decisively from the domain of technical compliance into the strategic priorities of hospital leadership. Institutions are recognising that cumulative radiation exposure, heavy protective equipment requirements, and associated staff fatigue are directly linked to burnout, physical injury, and talent attrition. In a market where experienced interventional cardiologists, cath lab nurses, and radiographers are difficult and expensive to recruit and retain, unsafe working environments carry direct financial and operational consequences.

As cath labs handle increasingly complex, lengthy procedures–TAVR, structural heart interventions, complex PCI, and peripheral vascular cases–cumulative imaging times are rising, increasing the risk of exposure for both patients and clinical staff. Traditional safety protocols are no longer adequate for this evolving procedural environment. Leading institutions are investing in advanced radiation shielding systems, AI-enabled low-dose imaging protocols, real-time personal dose monitoring, and enhanced visualisation tools that reduce exposure without compromising procedural efficiency or image quality.

Procurement evaluation criteria are evolving accordingly. Beyond imaging performance and throughput specifications, leading buyers now systematically assess dose-reduction capability, ergonomic design, staff-comfort features, and long-term workforce-protection benefits before approving capital expenditure. The strategic message for hospital leadership is clear–safer cath labs reduce burnout, improve staff retention, lower injury-related costs, and sustain long-term productivity. Radiation safety has become simultaneously a compliance requirement, a workforce economics issue, and a marker of future-ready healthcare infrastructure.

Software as the new competitive edge

For many years, cath lab competitive positioning was driven primarily by hardware–newer imaging systems, larger procedural suites, and premium equipment specifications. That equation is changing rapidly. The real differentiator in high-performance cardiology programs today is increasingly software. In high-volume environments, financial margin is frequently lost not during procedures themselves, but in the operational gaps surrounding them–scheduling bottlenecks, delayed documentation, missed charge capture, disconnected inventory systems, and underutilised room time. Even the most advanced imaging hardware cannot resolve these systemic workflow inefficiencies.

Modern digital cath lab platforms are converting operational friction into competitive advantage. Intelligent scheduling tools reduce room downtime, improve case sequencing, and increase daily throughput without requiring additional physical capacity. Automated documentation and structured clinical reporting shorten turnaround times, accelerate discharge workflows, and improve clinician productivity. Integrated charge capture systems reduce revenue leakage by ensuring devices, consumables, and procedural steps are accurately and completely recorded against each case.

Software is also transforming supply chain economics within the cath lab environment. Real-time inventory visibility prevents stockouts, reduces over-ordering, eliminates expired implant write-offs, and controls unmanaged device expenditure. With tighter cost controls and cleaner transactional data, administrators gain meaningful visibility into contribution margins by procedure type, treating physician, and room utilisation pattern–enabling more informed operational decisions.

The next frontier is analytics-driven performance management. Data-mature cath labs can benchmark turnaround times, complication rates, radiation exposure metrics, implant utilisation patterns, and physician productivity against internal targets or network-wide standards–creating a continuous performance improvement capability rather than a static procedural environment. Procurement priorities are shifting to reflect this reality. Hospitals are no longer purchasing standalone angiography systems–they are investing in integrated operating ecosystems that connect imaging, clinical reporting, inventory management, scheduling, billing, and analytics into a unified performance model. Interoperability, cybersecurity architecture, AI readiness, and scalability now carry significant weight alongside traditional detector quality specifications. The cath lab has entered a platform era–and software will increasingly determine which institutions lead it.

Consumables control profits

In modern cath labs, sustainable profitability is shaped as much by recurring consumable spend as by capital equipment investment. Balloons, stents, catheters, guidewires, sheaths, and contrast media generate continuous expenditure that can quietly and significantly erode procedure-level margins if left unmanaged. While hospital leadership typically focuses analytical attention on capital allocation decisions, the real financial pressure in established cath labs often originates from repeat consumable purchases that directly determine procedure economics.

Centralised procurement models are gaining strategic momentum as a response to this challenge. By consolidating purchasing across facilities or procedure types, hospital groups can secure more favourable pricing, improve supply continuity, reduce emergency buying premiums, and strengthen vendor accountability. Structured category management delivers scale benefits and cost predictability that fragmented, ad hoc procurement cannot achieve.

SKU rationalisation is an equally powerful financial lever. Many hospitals maintain excessive product variation within their consumable inventory, tying up working capital and increasing wastage. Standardising core product ranges and consolidating vendor relationships simplifies inventory management, improves utilisation rates, and lifts contribution margins without compromising clinical quality or physician preference. Fewer, deeper vendor partnerships also create clearer accountability and stronger negotiating positions. The next phase of cath lab financial performance will be determined in large part by institutions that treat consumables as a strategically managed spend category–not an administrative afterthought. Long after the initial capex commitment is made, consumable economics will determine whether the investment performs as expected.

Talent is capacity

The most binding constraint on cath lab expansion in India today is not capital equipment or physical infrastructure–it is qualified human capital. India’s growing cardiovascular disease burden is creating urgent, sustained demand for trained cath lab nurses, radiographers, cardiac technologists, and biomedical engineers capable of supporting an increasingly complex interventional environment. Without the right workforce in place, even technically advanced facilities consistently fall short of clinical capacity and consistency targets for outcomes.

Operator efficiency is fundamentally a team capability question. The performance of a skilled interventional cardiologist is directly dependent on the competence of the surrounding team–nurses who understand procedural sequencing, imaging staff who can optimise fluoroscopy settings in real time, and technicians who maintain equipment readiness and respond appropriately to clinical emergencies. Faster room turnaround, smoother procedural execution, and better patient experience all depend on coordinated, well-trained teams rather than individual clinical excellence alone.

Structured competency development is equally critical for patient safety and institutional risk management. Post-procedure monitoring protocols, complication recognition and response, infection prevention, radiation safety compliance, and equipment maintenance all require continuous, structured training rather than one-time orientation. Hospitals that invest in formal certification pathways, regular competency assessments, and ongoing professional development programmes consistently achieve stronger productivity metrics, lower adverse event rates, and greater staff retention. The next era of cath lab growth will be defined as much by investment in talent pipelines as by technology budgets. Workforce capability is cath lab capacity.

OEM wars begin

The cath lab competitive landscape is entering a new phase of intensity as traditional imaging OEMs face mounting pressure from software-led innovators and ecosystem-focused challengers. Established manufacturers continue to defend their positions through core hardware strengths–detector performance, image clarity, radiation efficiency, long-term reliability, and hybrid room capability. These remain critical evaluation criteria for hospitals making long-duration capital commitments. However, the competitive battleground is expanding rapidly beyond hardware performance alone.

Newer market entrants are gaining meaningful traction by offering smarter workflow tools, AI-enabled clinical analytics, modular upgrade pathways, faster system deployment, and decision-support platforms that improve operational efficiency without requiring complete system replacement. This is fundamentally changing how sophisticated buyers define and evaluate procurement value. Recent acquisitions and strategic partnerships across the sector demonstrate clear convergence between imaging devices, workflow software, and clinical data intelligence–with vendors racing to construct integrated ecosystems rather than continuing to compete on standalone product specifications.

For hospital leadership and healthcare investors, the key strategic question has shifted–it is no longer simply which manufacturer offers the best machine today–but which vendor has the strongest, most credible platform roadmap for the next decade. In the next major procurement cycle, systems selected for future-ready software architecture, interoperability, service depth, and upgrade flexibility may deliver superior long-term value compared to systems chosen solely on current technical imaging specifications.

AI in the cath lab – Promise, hype, and practical ROI

Artificial intelligence is entering the cath lab at an accelerating pace, but the narrative has matured significantly beyond early-stage excitement. A new generation of intelligent platforms promises meaningful clinical and operational benefits–faster lesion detection, enhanced image interpretation, automated structured reporting, radiation dose optimisation, predictive case scheduling, and more efficient procedural workflows. Rather than functioning as a futuristic overlay, AI is increasingly being embedded as an operational intelligence layer that helps clinicians make faster, better-informed decisions while reducing friction in high-volume procedural environments.

The greatest near-term potential lies in physiology-guided intervention and procedure planning. AI-powered FFR assessment tools, quantitative angiography analytics, stent optimisation software, and workflow intelligence platforms can help operators characterise lesion severity more accurately, select treatment strategies with greater confidence, and streamline complex PCI pathways. When well-integrated into existing clinical workflows, these tools can measurably shorten procedure times, improve room throughput, and support more consistent patient outcomes across operator experience levels.

However, hospitals are becoming considerably more sophisticated buyers of AI capability. The central evaluation question is no longer whether a platform sounds technologically impressive–it is whether it delivers quantifiable, attributable financial returns. Does it demonstrably reduce contrast agent consumption, limit radiation exposure, shorten delays, reduce repeat imaging episodes, ease staffing pressure, or eliminate clinically unnecessary stenting? Or does it primarily inflate the system acquisition cost with features that are rarely used after installation?

The next leaders in cath lab AI will be platforms that integrate naturally into clinical workflow, earn and sustain clinician trust, and generate hard, measurable financial and operational benefits. Adoption will ultimately be determined not by marketing claims, but by clear economic logic, practical efficiency gains, and reproducible clinical impact demonstrated in real-world settings.

The cath lab of 2030

By 2030, the catheterisation laboratory will have completed its transition from a specialty procedure room to one of India’s most strategically important healthcare assets. In metropolitan markets, hospital groups will develop multi-lab campuses and dedicated hybrid centres optimised for complex cardiac and vascular interventional programmes. In Tier-II cities, compact, high-throughput labs will compete on speed of access, operational efficiency, and leaner cost structures. In district and rural markets, mobile cath lab models and shared-capacity arrangements will progressively extend advanced cardiac care access to underserved populations.

Success in this environment will not be determined by expansion capacity alone, but by operational execution quality–the right geographic footprint, the right procedure mix, appropriate technology investment, trained and retained clinical teams, functioning referral networks, and integrated digital efficiency. Hospitals that successfully balance superior clinical outcomes with disciplined scheduling, consumable cost management, imaging productivity, and sustained patient trust will establish durable competitive positions.

For healthcare chains, cath labs will increasingly function as network growth engines–generating cardiology referral volumes, driving ICU demand, supporting diagnostics utilisation, and building regional brand equity simultaneously. The institutions that will lead Indian cardiac care through the next decade are not those that treat the cath lab as a capital acquisition–but those that manage it as an intelligent, continuously optimised, high-yield cardiovascular business platform.

Second opinion