CT Scanners

The evolving CT market

In the ever-evolving landscape of medical imaging, CT stands out as a cornerstone technology.

Computed tomography scanners have been very much in the news in India since October 15, 2024. They rank high among the most expensive pieces of equipment that any hospital or healthcare provider will invest into. In the face of budget constraints and the constant pressure to deliver superior patient care, hospitals are seeking cost-effective alternatives without compromising on quality and reliability. In fact, given the high cost of acquisition, many smaller facilities are forced to forego these key medical imaging assets altogether.

But there is a better way. What if the healthcare facility could acquire an advanced CT scanner at a significantly lower cost, without needing to compromise on quality or reliability? This is exactly what refurbished CT scanners from a trusted solution provider bring to the table, with a thorough inspection and certification process followed for each machine.

Refurbished medical equipment offers a compelling solution to this dilemma. By refurbishing pre-owned equipment to meet stringent quality standards, providers make cutting-edge technology accessible to healthcare facilities at a fraction of the cost of new machines. This not only helps hospitals optimize their capital expenditure but also enables them to invest in other critical areas of patient care and facility development.

Circling back to India in October. The Union Ministry of Environment, Forest, and Climate Change (MoEF&CC) issued on October 15, 2024, a pruned list of refurbished equipment that are allowed to be imported by hospitals reducing the items from 50 to 38 high-end and high-value machines, and this list includes CT scanners. While the decision was based on consultation with the Director General of Health Services (DGHS) in the union health ministry, the Indian manufacturing industry is up in arms. They protest that the development is a major setback for domestic manufacturing capabilities and India’s push toward self-sufficiency.

A number of domestic companies that manufacture products similar to those listed on the 2023 office memo made representations to various government departments, detailing their investments, manufacturing capabilities, and employment generation, along with lists of installations in India and overseas. They objected that equipment manufactured in India should not be allowed for import. On one hand, the government is promoting manufacturing of this equipment through production-linked incentive (PLI) schemes, and, on the other hand, allowing discarded medical devices by developed countries to be lapped up by Indian hospitals, said the manufacturers. Also, refurbished devices, which have undergone repairs and cosmetic updates, cannot replicate the functionality and reliability of new equipment. They are also not regulated by the country’s apex drug and devices regulator Central Drugs Standard Control Organization. Groups have now requested the Union Health Minister JP Nadda to intervene and rescind the policy.

There has been tremendous innovation, internationally. Here is a look at five of the latest significant trends shaping the scope of computed tomography in medical imaging.

Cardiac CT. Perfusion CT and coronary CT angiography (CCTA) are instrumental in assessing tissue perfusion, vascular abnormalities and hemodynamic changes. Perfusion CT plays a crucial role in stroke evaluation, tumor characterization, and assessment of vascular disorders. Advances in dynamic contrast-enhanced CT (DCE-CT) enable real-time assessment of tissue vascularity and pharmacokinetics, holding promise for personalized medicine and treatment monitoring.

Photon-counting CT represents a paradigm shift in CT detector technology. By directly counting individual photons rather than measuring their energy after interaction with scintillation materials, photon-counting detectors offer superior energy resolution, spatial resolution, and multi-energy capabilities. These detectors facilitate spectral CT imaging, enabling enhanced material decomposition, virtual non-contrast imaging and improved image quality at reduced radiation doses.

The convergence of radiomics and artificial intelligence (AI) is reshaping CT imaging analysis. Radiomics extracts quantitative data from medical images to characterize tissue properties and predict clinical outcomes. AI algorithms analyze vast datasets to identify patterns, classify abnormalities, and assist in diagnostic decision making by detecting abnormalities and quantifying disease burden. Integrating radiomics and AI into CT interpretation enhances diagnostic accuracy, enables predictive modeling, and facilitates personalized medicine approaches and treatment plans.

Dose reduction. With increasing concerns about radiation exposure in medical imaging, there is a continued emphasis on developing techniques to reduce radiation dose in CT imaging without compromising diagnostic accuracy. Innovations, such as adaptive dose modulation, optimized scanning protocols, and AI-driven dose reduction algorithms are helping to minimize radiation exposure while maintaining image quality and diagnostic confidence.

Portable and point-of-care CT. The integration of CT into point-of-care settings is a burgeoning trend, driven by the demand for rapid and accessible diagnostic imaging. Portable and compact CT scanners are being developed for use in emergency departments, intensive care units and remote healthcare facilities. These systems enable timely imaging, facilitating prompt diagnosis and treatment decisions. Point-of-care CT also holds promise for applications in resource-limited settings and telemedicine. A variety of medical imaging companies offer portable CT options.

Indian market dynamics

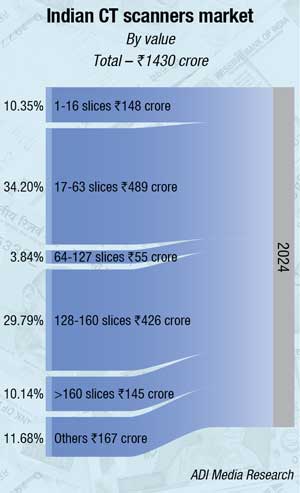

The Indian CT scanner market saw an exponential increase in the pandemic years, in 2020 and 2021. The market is estimated at ₹1950 crore in 2021, and a decline to ₹1680 crore with 1245 units in 2022, and a further decline to ₹1380 crore in 2023. In 2024, the trend reversed to 880 units, valued at ₹1430 crore. The number of units had declined, but the value increased, as the government has become more discerning. It has shifted preference from the ₹1.5-crore to ₹2-crore bracket to ₹4-crore models. Also, the new entrants are gaining entry by offering better payment terms.

Despite the expansion plans of most of the listed hospitals and the increase in the number of beds, the equipment is not seeing corresponding traction. Many healthcare providers are moving some of the equipment, CT scanners being one of them, from the existing facilities to the new expansion projects.

|

Leading players* |

|

| Tier I | Siemens & GE |

| Tier II | Philips and United Imaging |

| Others | Fujifilm (Hitachi), Toshiba (Canon), Schiller, Carestream, and Medirays; many new Chinese players including Neusoft have entered the market |

|

*Vendors are placed in different tiers on the basis of their sales contribution to the overall revenues of the Indian CT scanners market. ADI Media Research |

|

The market is dominated by GE, Siemens, and United Imaging. Philips is aggressive and in 2023 was awarded an order for 30 machines by the UP government for high-end machines. Fujifilm (Hitachi), Canon (Toshiba), and Schiller also have presence.

Technological advancements in CT scanner systems are driving innovation and shaping the market. Manufacturers are continuously improving scanner hardware, software, and imaging techniques to enhance diagnostic accuracy, image quality, and patient safety. Innovations, such as multi-slice CT scanners, dual-energy CT scanners, and spectral imaging capabilities enable healthcare providers obtain detailed anatomical and functional information with greater speed and precision. Advancements in artificial intelligence (AI) and machine learning algorithms are facilitating automated image analysis, workflow optimization, and decision support, further enhancing the clinical utility and efficiency of CT scanners. As technology continues to evolve, the adoption of advanced CT scanner systems is expected to increase, driving market growth and expanding the scope of diagnostic imaging applications.

CT scanners play a crucial role in cardiovascular imaging, offering non-invasive and rapid assessment of cardiac anatomy, function, and pathology. With the rising burden of cardiovascular diseases in India, including coronary artery disease, stroke, and heart failure, there is a growing demand for advanced imaging technologies to support early diagnosis, risk stratification, and treatment planning. CT coronary angiography (CTA) has emerged as a valuable tool for detecting coronary artery stenosis, assessing plaque burden, and guiding coronary interventions, offering high diagnostic accuracy and clinical utility. Cardiac CT imaging is increasingly being used for pre-procedural planning and post-procedural evaluation of structural heart interventions, transcatheter aortic valve replacement (TAVR), and electrophysiological procedures. The integration of CT scanners with advanced cardiac imaging techniques, such as myocardial perfusion imaging, cardiac calcium scoring, and functional assessment, further enhances their diagnostic capabilities and clinical value in cardiology practice.

With cancer incidence on the rise, and the need for early detection and personalized treatment strategies becoming increasingly important, the demand for CT scanners is growing. CT scans are used for tumor detection, characterization, and assessment of treatment response, providing valuable information for oncologists to guide treatment decisions and monitor disease progression. Advancements in CT imaging techniques, such as perfusion imaging, diffusion-weighted imaging, and dual-energy CT, enable the evaluation of tumor vascularity, tissue perfusion, and treatment efficacy, further enhancing the clinical utility of CT scanners in oncology.

CT scanners are finding increasing applications in the neurology segment. They diagnose neurological disorders, such as multiple sclerosis, Alzheimer’s, and dementia. CT scanning of the brain enables to differentiate the brain area affected by the disorder and is useful for differentiating vascular dementia from Alzheimer’s disease.

One of the primary challenges confronting the market is the high initial investment and ongoing maintenance costs associated with acquiring and operating CT scanner systems. The capital expenditure required to purchase state-of-the-art CT scanners, particularly advanced models with multi-slice capabilities and specialized imaging functionalities, can be prohibitively expensive for many healthcare facilities, especially smaller clinics and rural hospitals with limited budgets. The costs associated with installation, training, and ongoing maintenance contracts further add to the financial burden. These high upfront and recurring expenses pose a significant barrier to market entry and adoption, limiting access to advanced diagnostic imaging technologies in underserved areas and among economically disadvantaged populations. Addressing this challenge requires innovative financing options, government subsidies, and collaborative procurement models to make CT scanners more affordable and accessible to a wider range of healthcare providers.

Another critical challenge facing is the shortage of skilled personnel and training opportunities for operating and maintaining CT scanner systems. While the demand for diagnostic imaging services continues to grow, there is a scarcity of qualified radiologists, radiologic technologists, and biomedical engineers with specialized training in CT imaging techniques and protocols. The rapid pace of technological advancements in CT scanner systems requires ongoing training and professional development to ensure optimal utilization and performance. However, training opportunities and educational resources for CT imaging are limited, particularly in rural and remote areas where healthcare infrastructure and educational institutions are scarce. This shortage of skilled personnel and training hampers the effective deployment and utilization of CT scanners, leading to suboptimal imaging quality, longer wait times, and increased risk of errors and inefficiencies. Addressing this challenge requires investments in workforce development, capacity-building initiatives, and public-private partnerships to expand training programs and enhance the skills of healthcare.

Augmented by the investor-friendly initiatives of the Government of India, the PLI scheme has provided the necessary impetus to India’s vision of becoming a global manufacturing hub for medical devices. GE, Siemens, Trivitron, and Allengers are approved under the radiology and imaging medical devices segment of the PLI scheme.

In April 2022, Wipro GE HealthCare released its made in India, Revolution Aspire, at the company’s new medical devices manufacturing factory in Bengaluru. The company had invested ₹100 crore in the plant. In the same month, Siemens Healthineers inaugurated the new production line at its Bengaluru facility to manufacture computed tomography scanners, at an investment of ₹92 crore. In July 2024, Trivitron has launched Terrene CT scanner, manufactured at its facility located in Andhra Pradesh MedTech Zone, Visakhapatnam.

India needs to build a local ecosystem for the components that go into the hi-tech end products. About 70 percent of the components of the CT scanner that the companies manufacture in India still need to be imported.

Global market dynamics

The global market for computed tomography (CT) scanners was valued at an estimated USD 8.5 billion in 2023, and is projected to reach USD 12.8 billion by 2030, growing at a CAGR of 6.1 percent from 2023 to 2030, according to Research and Markets.

The increasing presence of CT scanners in healthcare settings has notably reduced hospitalization times and enhanced disease treatment across various indications. In addition, clinical facilities are focusing on upgrading and replacing outdated systems to improve patient care and treatment outcomes, which further boosts the adoption of CT scanners. Consequently, the expanding deployment of CT scanners in rural healthcare settings for imaging across multiple surgical fields, such as cardiovascular, orthopedics, and neurology has supported market growth.

Healthcare agencies at national and regional levels are promoting strategies like R&D investment and funding for national programs to expand the availability of medical devices for both healthcare providers and patients. These initiatives are expected to improve access to advanced imaging modalities in diagnostic centers, contributing to the expansion of the market.

Additionally, the rising demand for bedside imaging, home healthcare, and the use of CT scans for assessing the efficacy of post-interventional procedures, medical implants, and anatomical confirmations are also propelling the global CT market. Moreover, the growing frequency of medical implant procedures, driven by changing lifestyles and an aging population, may increase demand. The high success rate of CT scans across a range of applications fuels the global CT scan market.

However, the high costs associated with purchasing and maintaining medical imaging equipment pose a significant barrier to the global CT scanners market. The estimated acquisition cost of a 16-slice CT system is USD 285,000 to USD 360,000, with an annual maintenance cost of approximately USD 60,000 for basic models and up to USD 250,000 for high-end 128-slice scanners. This substantial maintenance expense makes it challenging for smaller healthcare facilities to afford these systems.

Additionally, the limited availability of robust maintenance policies for medical equipment and a shortage of qualified technical staff hinder the adoption of new devices across healthcare sectors.

Regional insights. In 2023, Asia-Pacific stood at USD 2.54 billion and is anticipated to grow at a higher CAGR, driven by the rising incidence of chronic diseases, a developing healthcare sector, and a strong unmet demand for advanced diagnostic systems in diagnostic centers. Furthermore, the region’s large and aging installed base of equipment in need of replacement creates substantial potential for new systems.

North America held a significant share of the global computed tomography (CT) scanners market in 2023. The growing number of patients undergoing diagnostic imaging procedures, combined with the increasing introduction of technologically advanced systems across US healthcare settings, has fuelled market growth in this region.

The imaging evolution

Computed tomography continues to evolve and is driven by technological innovations and clinical demands. From advancements in image reconstruction algorithms to the integration of photon-counting detectors, the landscape of CT imaging is marked by continuous progress. These trends hold the promise of improving diagnostic accuracy, reducing radiation exposure, and expanding the clinical utility of CT across diverse medical specialties. As we navigate the future of medical imaging, computed tomography remains at the forefront, shaping the way we visualize and understand the human body.

Second Opinion

Photon counting CT – A promising novel technique with emerging applications.