MRI Equipment

MRI’s next decade – From magnet to medical intelligence engine

MRI evolves into an AI driven, cloud native platform at the core of precision medicine.

Magnetic resonance imaging has reached a pivotal inflection point. No longer just a diagnostic scanner, it is evolving into an intelligent ecosystem that fuses advanced magnet technology, embedded AI, and cloud-native digital health infrastructure. Surging demand for high-resolution imaging, early disease detection, and precision medicine is forcing providers to reimagine MRI’s role in clinical pathways. Today’s platforms do more than capture images–they compress scan times, automate complex analysis, and generate actionable, quantitative insights that support sharper, faster, and more consistent diagnoses across service lines.

This transformation is powered by simultaneous breakthroughs in hardware, software, and data. Next-generation superconducting magnets and gradients improve field stability, spatial resolution, and throughput, while AI-enhanced reconstruction and protocol optimization shorten scan times and enhance image clarity. Cloud-connected architectures enable remote radiologist collaboration, multi-site imaging orchestration, and real-time access to advanced analytics, accelerating decision-making across hospital and diagnostic networks. MRI is graduating from an isolated box in the corner suite to a connected diagnostic powerhouse at the center of digitally enabled care.

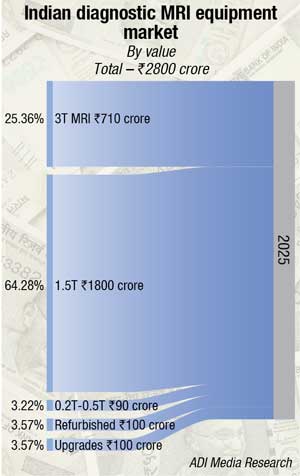

Indian market dynamics

The Indian MRI market in 2025 is estimated at ₹2800 crore.

United Imaging is gaining traction in India’s MRI market, anchored by its ₹2,500 crore Superhealth contract to equip 100 zero wait time hospitals with MRI, CT, cardiac CT, x-ray, and mammography systems under a full-lifecycle model. The October 2025 deal positions it as a credible challenger to GE, Siemens, and Philips in greenfield projects, even as incumbents retain dominance in installed base and government business through financing, managed services, and PPP models. With competitive high field MRI offerings, United Imaging (with support from Medikabazaar ) and Canon are putting pressure on mid-tier segments, squeezing domestic OEMs that compete primarily on price.

| Leading players* 2025 |

|

| Tier I | Siemens, Philips, & GE |

| Tier II | United Imaging |

| Others | Fujifilm, Canon, Hitachi, Erbis, Bruker, Esaote, Shimadzu, Blue Star, Time Medical, Voxelgrid, and Sanrad |

| *Vendors are placed in different tiers on the basis of their sales contribution to the overall revenues of the Indian MRI equipment market.

ADI Media Research |

|

At the field-strength level, 1.5T platforms remain the workhorse, with a 67 percent share, constrained by infrastructure and power realities. This segment is gaining strong traction as providers look for reliable, cost-effective imaging to manage neurological, musculoskeletal, and oncological workloads. Growing from this demand base, the 1.5T segment is projected to expand at about 11 percent CAGR through 2036, with India already accounting for nearly 22 percent of the APAC MRI systems market in 2025. Domestic, AI-enabled, Made in India platforms are further improving workflow, patient comfort, and affordability, supporting wider adoption across radiology departments and imaging centres, and reinforcing a robust long-term outlook for the segment. On the other hand, ≥3T scanners are concentrated in tertiary and academic centers and are growing faster off a smaller base.

Neurology accounts for the largest share of MRI applications, at around two-fifths, followed by oncology at nearly one-fifth, with cancer imaging showing the highest growth due to wider adoption of multiparametric protocols, particularly in prostate and breast cancer.

On the demand side, hospitals generate just under half of MRI revenues, anchored by emergency and inpatient referrals, while standalone clinics and diagnostic chains contribute a bit over one-third and are scaling faster via franchise and asset-light models in Tier-II and Tier-III cities. Utilisation is rising for cardiovascular, cancer, diabetes, and neurodegenerative conditions, supported by Ayushman Bharat, NHM, and improved MRI reimbursement, which collectively improve project viability in smaller towns and public facilities.

Technology trends–AI-enabled protocols, faster sequences, and tele-reporting–are lifting throughput and radiologist productivity, strengthening the economics of new rooms and upgrades. In parallel, helium-free and helium-light architectures are emerging as a major technology theme, with both OEMs and startups introducing conduction-cooled or dry-cooled magnets that either use almost no liquid helium or eliminate it altogether. An important angle is that technology is no longer synonymous with high-end metro-only 3 T installations; it increasingly means AI upgrades on existing 1.5 T fleets, low-helium or helium-free magnets that simplify operations in smaller cities, and indigenous systems that change the procurement math for public tenders and PPP projects.

Structurally, India’s first indigenous MRI platform, launched around 2025, aims to cut acquisition cost and reduce import dependence, paving the way for deeper penetration into district and rural markets over the medium term.

Make in India and PLI incentives are accelerating domestic 1.5T development, with some forecasts suggesting that by 2030, up to half of incremental shipments could be locally manufactured, adding pricing pressure and greater customisation for Indian use cases. Within Asia-Pacific, India already accounts for just over one-fifth of MRI system demand, underscoring its status as one of the region’s fastest-growing MRI markets.

Rising geopolitical instability in West Asia is now impacting helium supplies, sending shockwaves through India’s MRI ecosystem. With helium–critical for MRI cooling–facing acute shortages, input costs are rising, and scan prices may follow, potentially delaying timely diagnosis. India’s heavy dependence on imports from Qatar, which accounts for nearly a third of global helium supply, has intensified the challenge, leading to constrained inventories and volatile logistics. The impact is beginning to spill over into the broader medical device sector, with concerns emerging around continuity of essential hospital consumables.

Amid this uncertainty, innovation is gaining traction, as several companies accelerate the development of helium-free MRI systems to reduce dependency and ensure service reliability. While promising, widespread adoption will take time, making supply stability a near-term priority for both industry and policymakers.

Making MRI more accessible – Compact, wide-bore, and silent MRI solutions for Tier-II/III cities and patient-centric care

Shunsuke Honda

Shunsuke Honda

Sr Manager – Medical Division,

FUJIFILM India Pvt. Ltd.

MRI has long been considered an indispensable tool in modern diagnostics, offering high-resolution visualisation of soft tissue without ionizing radiation. Yet, despite its importance, access to MRI remains limited in many regions, particularly in smaller cities where infrastructure and installation requirements pose significant barriers.

Traditionally, MRI systems required large installation spaces, specialised site planning, and infrastructure investments, which can be difficult for smaller healthcare centres. In recent years, however, the industry has been steadily shifting towards more compact system designs. Modern MRI systems incorporate a low helium magnet, cryostat insulation, and optimised coil geometry, allowing magnets to maintain stable field strength while reducing overall system size. In addition, advances in electronics miniaturization have enabled gradient amplifiers and RF components to be more tightly integrated within the scanner architecture. Such advancements enable smaller footprints and simplified installation, making MRI accessible in tier-II and tier-III cities.

Alongside accessibility, patient centric experience has become a growing focus. For many patients, undergoing an MRI examination can be stressful due to the narrow bore design of scanners and the loud acoustic noise generated during imaging sequences. MRI scanners typically featured a bore of around 60 cm, creating a sense of confinement, particularly for claustrophobic or anxious patients. In response, many wide-bore design with opening of 70 cm have emerged by creating a more open and comfortable scanning environment while still maintaining high magnetic field homogeneity and image quality also making MRI more tolerable for broader range of patients including elderly individuals and paediatric cases.

Noise reduction is another important advancement in modern MRI systems. The loud knocking sounds commonly associated with MRI are generated by rapid switching of gradient coils often exceeding 100 decibels. To address this, modern MRI systems incorporated improved gradient coil design, vibration damping & acoustic insulation. Optimized pulse sequences further reduce gradient switching intensity contributing to quitter & more comfortable experience.

Overall MRI is evolving beyond performance alone toward accessibility and patient experience. Compact designs, wider bore, and quitter imaging environments are expected to play a key role in expanding diagnostic services beyond major urban centres.

A 10-year-old MRI is exactly at the point where OEMs and hospital guidelines recommend either a full replacement or a comprehensive technology refresh, so choosing a magnet-retaining upgrade is a financially and operationally sound decision if the existing magnet and room are in good condition. By reusing the magnet and much of the existing infrastructure, a modern upgrade can extend the system’s life by another 7–10 years. It can also deliver near–current-generation image quality and faster scan speeds. At the same time, it helps avoid the high capital expenditure, extensive civil work, and long downtime required for a completely new scanner. This is why several leading Indian hospital groups are quietly shifting to rapid, high-end CT and MRI platforms. These systems enable five-to seven-minute scans and advanced 3D imaging. Importantly, hospitals can offer these improvements without proportionately increasing scan prices for patients.

At the beginning of 2025, CDSCO wrote to Customs that pre-owned and refurbished medical devices, including MRI and CT, cannot be imported for sale or distribution because there is no licensing pathway for them under the Medical Devices Rules, 2017, and Customs was advised not to clear such consignments. This effectively slowed the refurbished high-end imaging market, even though MoEFCC had already notified (and later updated) a list of 38 refurbished high-value devices such as MRI, CT and PET-CT that could be imported under waste-management and reuse rules, creating a policy contradiction between environmental approvals and medical-device regulation.

For the domestic MRI market, this means a real supply problem: refurbished systems were a critical way to create capacity in Tier-II and Tier-III cities where a brand-new ESOP-level scanner is financially unviable for many stand-alone centres and small hospitals, so access and geographical reach are now being hit at exactly the time when the government wants more diagnostics closer to where people live. India still has relatively few MRI units for its population, Make in India efforts around high-end magnets and indigenously built MRI scanners are at a very early stage with limited capacity, and even with new schemes for rare-earth magnet production the ecosystem will take time to scale, so a blanket closure of the refurbished import route in the 5-to 10-year age band risks worsening both affordability and availability in the medium term.

From a policy point of view, the government’s concerns about quality and patient safety are valid, and a completely unregulated refurbished market is not acceptable, but instead of an implicit ban the system needs a clear, transparent regulatory pathway under the Medical Devices Rules that links import permission to objective quality-control requirements: age limits that reflect actual MRI lifecycle practice (for example, minimum five years in first use but maximum total age or scan-hour thresholds), documentation and audit of original OEM refurbishment standards, evidence of post-refurbishment testing and safety checks, and minimum criteria for the size, capability and quality-systems of companies allowed to refurbish and supply. In short, if India wants both Make in India and mass access to advanced diagnostics, refurbished MRI and other high-end devices have to be brought under a robust, fit-for-purpose regulatory framework rather than being pushed into a grey zone; this would allow safe imports of systems older than five years that no one replaces in India anyway, while protecting patients and giving Customs and hospitals clear rules to follow.

Global market scenario

Global health systems are investing heavily in next-generation MRI platforms. The global MRI equipment market is projected to grow from about USD 8.57 billion in 2026 to USD 14.02 billion by 2034, at a CAGR of more than 6 percent, driven by the rising burden of chronic and complex diseases and the need for advanced diagnostics. Hospitals, imaging centers, and research institutions are upgrading fleets for neuro, oncology, cardiovascular, and musculoskeletal applications–prioritizing workflow efficiency, lifecycle cost optimization, and enhanced patient experience rather than simply adding raw scanner capacity.

MRI remains a core modality within modern imaging strategies, offering high-resolution, radiation-free visualization for neurology, oncology, cardiovascular medicine, musculoskeletal conditions, and abdominal disorders. Rising prevalence of neurological diseases, cancer, and degenerative musculoskeletal conditions is amplifying the demand for sophisticated MRI systems that can deliver precise disease detection, staging, and longitudinal monitoring.

Technological advances in magnet design, gradients, and software are reshaping the market mix. While 1.5T platforms still represent a large installed base, clinical demand is clearly drifting toward 3T systems and, in selected centers, ultra-high-field 7T scanners for highly specialized applications. Higher field strengths provide superior signal-to-noise ratio and spatial resolution, enabling detection of subtle anatomical and microstructural changes and early disease markers that were previously invisible. Once confined largely to research environments, ultra-high-field systems are increasingly being translated into advanced neurological and oncological clinical practice.

Artificial intelligence is emerging as a critical growth accelerator. AI-powered reconstruction, motion correction, automated protocol selection, and automated post-processing are cutting scan times while preserving or even improving image quality. This unlocks higher patient throughput, more consistent examinations across technologists and sites, and reduced variability in interpretation. AI is progressively being embedded directly within MRI consoles and radiology workflows to assist with anomaly detection, segmentation, and quantification, reducing radiologist workload and supporting more reproducible, data-rich reporting.

Hardware innovation is advancing in parallel. Major vendors are moving aggressively toward helium-efficient and helium-free magnet technologies, using sealed designs that minimize or eliminate helium refills. These systems reduce installation complexity, avoid dependence on volatile helium supply chains, and lower total cost of ownership–benefits that are particularly attractive for emerging markets contending with infrastructure constraints. Such designs also support more compact footprints, enabling MRI deployment in space-constrained urban sites and smaller hospitals.

Patient-centric design is another defining trend. Wider and shorter bores, quieter gradients, faster sequences, and motion-resilient protocols are reducing patient anxiety and discomfort, lowering the need for sedation, and decreasing repeat scans due to motion. In parallel, low-field and portable MRI–often enhanced by AI-based reconstruction–is extending access to emergency departments, ICUs, and remote or resource-limited settings, where quick, bedside imaging can be life-saving.

The broader MRI ecosystem now encompasses much more than scanners. Coils, gradients, software stacks, AI applications, service and maintenance contracts, and workflow optimization solutions are critical components that determine clinical performance and economic viability. Global OEMs share the field with regional innovators, especially in areas like portable MRI, AI software, and specialized coils, intensifying competition and innovation.

Structural challenges remain–high capital costs, demanding infrastructure, and historically long scan times have limited adoption in some developing regions. However, AI-enabled efficiency gains, helium-free designs, flexible financing, and public–private partnerships are progressively lowering these barriers and unlocking new markets.

Regional dynamics

Regional MRI markets are fragmenting along lines of infrastructure maturity, reimbursement, and technology readiness. According to recent analyses, Asia-Pacific accounted for roughly 46 percent of the global MRI equipment market in 2025, reflecting rapid adoption of advanced imaging systems, expanding hospital networks, and rising chronic disease burden in countries such as China, Japan, and India. North America, meanwhile, remains a technology and revenue leader, with around 38–44 percent share of the MRI systems market depending on the source, underpinned by high healthcare expenditure, large imaging volumes, and rapid uptake of 3T and AI-enabled systems.

North America’s strength lies in its advanced healthcare infrastructure, strong presence of major imaging OEMs, and emphasis on early and preventive diagnostics. High scanner density and favourable reimbursement support continuous replacement of ageing systems with high-field and AI-integrated platforms. These factors ensure continued leadership in the deployment of innovation and clinical research.

Asia-Pacific is emerging as the fastest-growing region. Rising healthcare spending, expansion of hospital and diagnostic networks, and government investment in diagnostic infrastructure are fuelling scanner installations across both urban and semi-urban geographies. India, in particular, is seeing strong MRI demand driven by neurological, spinal, and orthopaedic conditions, with private hospital chains and diagnostic networks extending MRI beyond metros into Tier-II and Tier-III cities. Policy levers, including production-linked incentives and support for domestic manufacturing, are encouraging local production of MRI components and systems.

MRI market–Tech titans rule

Expert consensus points toward a clear bifurcation of the MRI market. Mid-field systems are gradually commoditizing, while high-field 3T and ultra-high-field platforms are becoming the key arenas for differentiation and value creation. Hospitals, academic centers, and research institutes are prioritizing systems that can support advanced neuroimaging, quantitative imaging, and seamlessly integrated AI, even if they come at a higher upfront cost, because they unlock superior clinical capabilities and research opportunities.

In this environment, competitive advantage shifts from pure hardware accumulation to integrated technology stacks. Vendors that combine high-performance magnets, embedded AI, advanced software, sustainable magnet technology, and scalable digital platforms will define the next generation of market leaders. MRI is evolving from equipment purchase to long-term digital partnership, with platforms serving as central intelligence hubs that connect imaging, analytics, and broader digital health ecosystems.

Next-gen magnet powerhouses

At the core of every MRI system lies its magnet, whose strength, homogeneity, and stability determine image quality, scan speed, and overall clinical capability. Superconducting magnet technology–long the backbone of MRI–continues to advance, with both low-temperature and emerging high-temperature superconductors driving field strengths from standard 1.5T and 3T into ultra-high-field 7T and beyond. These advances, combined with more powerful gradient systems, are pushing spatial and temporal resolution to new heights, revealing subtle anatomical details across neurological, oncological, cardiac, and musculoskeletal imaging.

A major focus of magnet innovation is sustainability and operational simplicity. Vendors are increasingly deploying sealed, cryogen-lite or cryogen-free magnet designs that drastically reduce or eliminate the need for liquid helium. Integrated sensor networks, remote monitoring, and AI-based system protection improve uptime and safety, including during power loss. The result is simplified installation, reduced infrastructure dependency, fewer maintenance interventions, and attractive lifecycle economics for hospitals and diagnostic centers.

Compact magnet architectures, made possible by these advances, enable MRI installations at sites previously considered infeasible–densely built urban hospitals, smaller regional centers, and specialized labs with limited space. For markets like India, this aligns well with policy initiatives that support local manufacturing and wider geographic distribution of advanced imaging through incentives and regulatory facilitation. The combination of compact, helium-efficient magnets and supportive industrial policy promises to accelerate MRI penetration into underserved geographies.

The helium-free revolution–MRI’s green upgrade

Historically, MRI systems have relied on large volumes of liquid helium to cool superconducting magnets to cryogenic temperatures. Helium is scarce, expensive, and vulnerable to supply disruptions, with traditional systems requiring complex venting and safety infrastructure. These dependencies translate into high installation costs, operational risks, and environmental concerns.

Helium-efficient and helium-free magnet technologies are now fundamentally changing this equation. By sealing small amounts of helium within the magnet or eliminating it entirely using cryocooler-based systems and specialized superconducting materials, vendors are delivering systems that maintain high performance with minimal to zero helium replenishment. This reduces environmental impact, cuts running costs, and removes a critical supply-chain vulnerability. It also simplifies facility requirements, allowing MRI to be deployed more flexibly in both mature and emerging markets.

These sustainable magnet platforms are often more compact and energy-efficient, supporting installation in smaller hospitals, community imaging centers, and new clinical frontiers. As helium constraints recede, industry R&D can refocus more heavily on advancing field strength, gradient performance, and new imaging capabilities, rather than being constrained by cryogen logistics.

Ultra-high-field MRI and parallel transmission–Power unleashed

MRI is advancing into ultra-high-field territory with 7T systems and beyond, which provide unprecedented spatial resolution and tissue contrast compared with 1.5T and 3T scanners. These systems reveal microstructural details and subtle pathology, particularly in neuroimaging, epilepsy evaluation, neurodegenerative disease research, and complex oncological applications. Clinicians gain deeper insight into cortical and subcortical structures, small lesions, and early disease signatures that were previously undetectable.

Parallel transmission (pTx) is a key enabling technology at these field strengths. By using multiple independent RF transmit channels, pTx helps overcome radiofrequency inhomogeneity that can otherwise mar image quality at ultra-high fields. It improves signal uniformity, reduces artifacts and local hot spots, and enhances both safety and diagnostic quality, allowing the full potential of 7T systems to be realized in clinical workflows. Together, ultra-high-field magnets and pTx unlock ultra-detailed views of brain architecture, subtle lesions, and tissue properties, feeding high-precision surgical planning and advanced disease characterization.

As field strengths rise and advanced sequences proliferate, the volume and complexity of MRI data grow exponentially. This data deluge is spurring rapid adoption of AI-driven reconstruction and analysis tools, along with the deployment of robust computational infrastructure, to ensure that ultra-high-field imaging translates into timely, actionable clinical decisions rather than data overload.

AI storming the MRI workflow

Artificial intelligence is transforming MRI from acquisition through to interpretation. Traditional MRI exams were often lengthy and complex, with protocol selection, parameter tuning, and post-processing demanding significant technologist and radiologist effort. Deep learning–based reconstruction now allows high-quality images from heavily undersampled data, shortening scan times while preserving or improving diagnostic quality. AI-driven motion correction and denoising further improve robustness, particularly in uncooperative or critically ill patients.

Beyond the scanner, AI streamlines the entire workflow. Intelligent systems assist with automated patient positioning, sequence selection, and real-time image quality assessment, reducing variability and improving consistency across sites. In post-processing, AI algorithms support lesion detection, segmentation, classification, and quantification, helping radiologists manage growing workloads and complex multi-sequence exams. These capabilities improve confidence, reduce reporting times, and facilitate more standardized, data-rich reporting that integrates easily into clinical decision support and research pipelines.

Foundation models–Universal imaging brainpower unleashed

AI in medical imaging is entering a new phase with foundation models–large-scale, generalizable models trained on massive multimodal datasets that may include MRI, CT, PET, ultrasound, clinical documentation, genetic data, and more. Unlike narrow, task-specific algorithms, foundation models learn broad anatomical and pathological representations and can be adapted to a wide range of tasks, including reconstruction, segmentation, anomaly detection, and outcome prediction.

For MRI, foundation models provide a powerful layer of intelligence atop increasingly complex imaging. They can fuse MRI data with physiological and molecular information, identify subtle imaging biomarkers, and generate highly personalized risk profiles and treatment recommendations. As data volumes from high-field scanners, advanced functional and metabolic imaging, and population-scale studies continue to grow, these models become essential for extracting clinically meaningful insights at scale.

Radiology AI ecosystems–Industry explosion

The rise of AI is catalyzing the emergence of comprehensive radiology platforms that span multiple imaging modalities. Large software vendors and imaging OEMs are building integrated AI ecosystems that embed a wide portfolio of algorithms directly into PACS, viewing workstations, and reporting systems. For MRI–which often produces multi-sequence, high-dimensional datasets–these platforms are especially valuable in orchestrating automated detection, segmentation, characterization, and triage in a unified environment.

Instead of isolated algorithms, health systems are adopting platform-based approaches that allow rapid deployment, updating, and governance of many AI tools simultaneously. Cloud-based architectures enable centralized model hosting, continuous upgrades, and cross-site scaling, ensuring that new AI capabilities are quickly disseminated across networks. These platforms address rising imaging volumes, radiologist shortages, and the need for consistent quality by acting as digital assistants that pre-screen cases, highlight potentially critical findings, and standardize quantitative measurement.

Cloud-native MRI platforms–Data infrastructure revolution

Cloud computing is becoming central to MRI data management and analysis. High-resolution 3D, 4D, and ultra-high-field datasets are straining traditional on-premise storage and compute infrastructures. Cloud-native imaging platforms enable organizations to offload storage, reconstruction, visualization, and AI-driven analytics to scalable, centralized environments. This approach provides elastic compute resources, faster upgrades, and easier integration of advanced applications without repeated capital-intensive hardware investments on-site.

Cloud-enabled workflows also transform collaboration. Radiologists, subspecialists, and multidisciplinary teams can access MRI studies securely from any location, facilitating remote reporting, second opinions, and tele-radiology. Zero-footprint viewers and cloud PACS remove the need for heavy local installations, while AI services running in the cloud can automatically analyze incoming studies, flag urgent findings, and deliver quantitative outputs to clinicians in near-real time. As cloud platforms integrate with electronic health records and research databases, MRI data becomes a core component of broader precision-medicine ecosystems.

MRI as a therapeutic powerhouse

MRI is extending beyond diagnostics into real-time guidance for therapy. MRI-guided radiotherapy platforms combine high-quality soft-tissue imaging with linear accelerators, allowing clinicians to visualize tumours and organs continuously during treatment. This enables adaptive radiotherapy, where plans are adjusted between or even during sessions based on real-time anatomy, improving target coverage and sparing healthy tissue, especially in mobile organs such as the lung, liver, and pancreas.

Interventional MRI is also gaining momentum, with MRI-compatible robotics, catheters, and navigation systems enabling biopsies, ablations, and other minimally invasive procedures under live imaging. These tools provide high-resolution visualization without ionizing radiation, supporting safer and more precise interventions in neurology, oncology, and musculoskeletal care. As robotics, AI navigation, and real-time imaging mature, MRI is positioned to become a central platform for both diagnosing and treating complex disease.

Neurological breakthroughs–MRI’s brain revolution

Neurology remains one of the fastest-advancing MRI frontiers. High-field and ultra-high-field systems, combined with advanced sequences such as diffusion, susceptibility-weighted imaging, and quantitative mapping, are allowing clinicians to detect microstructural changes associated with epilepsy, dementia, Parkinsonian syndromes, and developmental disorders that were previously occult. These capabilities improve diagnostic accuracy, especially for patients with subtle or focal abnormalities.

In epilepsy, for example, high-resolution imaging can reveal previously undetected lesions or cortical dysplasias in drug-resistant patients, guiding surgical planning and improving outcomes. In neurodegenerative disease, quantitative MRI can characterize microstructural and functional changes that precede overt atrophy or clinical symptoms, thereby enabling earlier detection and targeted intervention. Large-scale neuroimaging cohorts and international collaborations are generating unprecedented datasets that map brain structure and function across the lifespan, fuelling both basic neuroscience and clinical innovation.

Population-scale MRI–Preventive health game-changer

Population-based imaging initiatives are harnessing MRI to understand disease trajectories and ageing at scale. By combining MRI data from tens or hundreds of thousands of participants with genomics, clinical records, and lifestyle information, researchers can identify subtle imaging markers that predict future disease, well before symptoms arise. These studies cover multiple organ systems–from brain and heart to vasculature and musculoskeletal structures–providing a holistic view of health and disease evolution.

Longitudinal MRI of large cohorts allows early detection of cardiovascular risk, neurodegenerative changes, and emergent cancers, positioning imaging as a cornerstone of preventive and predictive medicine. The massive datasets generated also serve as training grounds for new AI and machine learning models, which can automate image analysis, discover novel biomarkers, and refine risk scores. However, realizing the full potential of population-scale MRI requires robust data infrastructure, privacy-preserving data sharing, and powerful analytical platforms capable of handling petabyte-scale information.

Machine learning–MRI innovation rocket fuel

Machine learning is helping overcome longstanding technical limitations in MRI. Advanced algorithms improve reconstruction from under sampled data, suppress noise, and correct for motion, allowing faster scans and more reliable imaging in real-world clinical conditions. These methods effectively extract more information from the same raw data, enhancing image quality without necessarily requiring hardware upgrades.

Beyond reconstruction, deep learning models can approximate high-field image quality from lower-field data, extending high-end performance to sites with older or lower-spec equipment. This virtual upgrade potential supports more equitable access to advanced imaging. Machine learning also underpins novel applications such as multimodal fusion, predictive models of disease progression, and exploratory research in areas like brain–computer interfaces, emphasizing MRI’s role as both a clinical and research platform in the broader AI and neuroscience ecosystem.

MRI in the era of neurotechnology and digital medicine

MRI is becoming foundational to emerging neurotechnology and digital medicine. High-resolution structural and functional imaging underpins the design and validation of brain–computer interfaces, neuromodulation therapies, and neuroprosthetics. Detailed maps of brain connectivity and activity patterns guide where and how neurotechnology interventions are targeted, and MRI is crucial for monitoring their effects over time.

In digital medicine, MRI-derived anatomical and physiological data are increasingly combined with other data streams to build digital twins of individual patients. These computational models can simulate disease progression, test virtual interventions, and inform personalized treatment strategies. As computing power and AI capabilities grow, MRI will provide high-fidelity ground truth for these models, ensuring that virtual predictions remain anchored in real patient biology.

MRI’s explosive decade ahead

The coming decade will be one of the most transformative in MRI’s history. Advancements in magnet technology, AI, cloud infrastructure, and interventional and neurotechnology applications are converging to turn MRI systems into intelligent, networked engines of precision medicine. These platforms will not only produce exquisite images but also decode disease signatures, guide real-time therapies, and support predictive and preventive care at the population scale.

As imaging merges with data science and digital health platforms, MRI will cement its role as a central, indispensable backbone of modern healthcare–reshaping how clinicians detect, characterize, and ultimately combat disease across the continuum of care.

Second opinion

Expanding MRI access across smaller Indian cities.

MRI equipment selection – Key considerations for hospitals and diagnostic centres.