HPLC Systems

From analyzer to asset – HPLC’s strategic reinvention in Indian labs

HPLC is powering precision, throughput, and ROI in India’s diagnostics revolution.

High-performance liquid chromatography (HPLC) has travelled a long way from its origins as a pharmaceutical quality-control workhorse. Today, it sits at the intersection of healthcare, life sciences, and advanced manufacturing, anchoring workflows in clinical diagnostics, therapeutic drug monitoring, toxicology screening, nutraceutical validation, food safety, biomedical research, and increasingly sophisticated hospital laboratory networks. Its unmatched ability to separate, identify, and quantify compounds in complex biological and chemical matrices has made it indispensable wherever precision, traceability, and turnaround time directly influence patient outcomes–or commercial value.

What began as a niche analytical tool has quietly become a strategic asset on the laboratory balance sheet. From verifying active ingredients in nutraceuticals to detecting biomarkers in oncology patients, HPLC now underpins decisions worth billions of dollars in the global health economy. The technology is no longer evaluated purely on chromatographic performance–it is being assessed as a productivity asset, a compliance enabler, and increasingly, a digital platform.

For India, where diagnostic volumes are scaling faster than skilled manpower, this shift is more than an upgrade cycle–it is a structural change in how laboratories invest, operate, and compete. As 2026 unfolds, the conversation around HPLC has decisively moved past resolution and sensitivity. It is now about automation, artificial intelligence, predictive maintenance, digital compliance, sustainability, and seamless integration with laboratory information systems. Welcome to the decade of intelligent chromatography.

Indian market dynamics

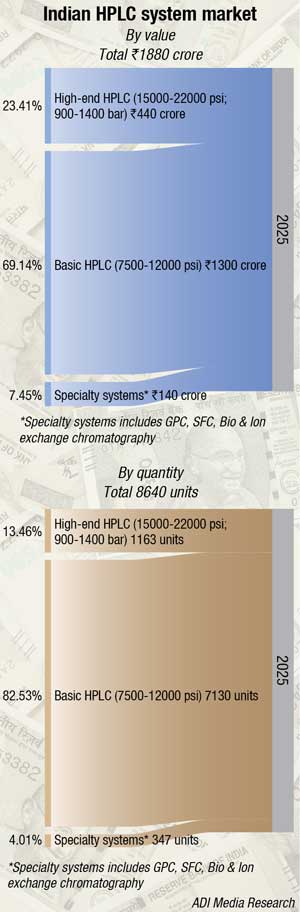

The Indian HPLC market is estimated at ₹1880 crore in value and 8640 units in number in 2025. This represents a measured but steady growth trajectory following the strong momentum of 2024, when the market crossed ₹1,750 crore and posted volume growth exceeding 13 percent. The tempered growth rate reflects buyer hesitancy stemming from US trade policy uncertainty in early 2025, which led to measurable deferrals of capital equipment purchases – particularly among export-oriented pharmaceutical manufacturers awaiting clarity on tariff exposure. That uncertainty has partially resolved, and procurement decisions deferred from Q1 2025 are now beginning to materialize in the order books.

The Indian HPLC market has become the strategic priority for global vendors precisely because their traditional markets are stalling. In the US and Europe, pharma R&D cost-cutting, the biotech funding winter, tighter academic budgets, and a post-pandemic CapEx normalization have all softened demand for instruments. Indian generics pricing pressure has further dampened Western quality control (QC) expansion.

|

Leading players* 2025 |

|

| Tier I | Shimadzu, Waters and Agilent |

| Tier II | Thermo Fisher |

| Others | PerkinElmer; Wufeng, Skyray, Techcomp; Analytical Technologies, Spinco, and Chemito |

| *Vendors are placed in different tiers on the basis of their sales contribution to the overall revenues of the Indian HPLC systems market.

ADI Media Research |

|

India offers the opposite picture. Pharma generics, a booming CDMO/CRO base benefiting from China-plus-one, biosimilars, and PLI-driven API investment, are all expanding simultaneously. USFDA, EDQM, and CDSCO scrutiny is driving continuous QC upgrades, while food safety mandates under FSSAI, environmental monitoring, agrochemical testing, and nutraceutical exports are further broadening demand. The result is one of the few double-digit-growth HPLC markets globally.

Every major vendor is chasing this growth at once, and that is what’s compressing prices. Agilent, Waters, Shimadzu, Thermo Fisher, and PerkinElmer are deploying India-specific SKUs, local assembly, consumables-inclusive bundles, and extended warranties to defend share. Shimadzu Corporation, for instance is making a decisive push into the Indian market, anchored by its new Karnataka-based manufacturing subsidiary (SMI) launching in spring 2027 and the recent consolidation of its analytical and medical sales arms into Shimadzu India Private Limited (SIP). With local production of HPLC, LC-MS, and GC-MS systems on the horizon – a first for any major global analytical instrumentation brand in India – the move signals a strategic bet on the country as both a manufacturing hub and a high-growth market for scientific instruments. Chinese entrants like Wufeng, Skyray, and Techcomp brands are attacking the value segment, forcing further response. Domestic players such as Analytical Technologies, Spinco, and Chemito are squeezed too, though they retain a service-proximity edge.

Green by method – HPLC’s sustainable future

Bhaumik Trivedi

Bhaumik Trivedi

Dy Manager Business Development-Clinical & Diagnostics,

Shimadzu India Pvt. Ltd.

High Performance Liquid Chromatography (HPLC) has long been the analytical workhorse of India’s pharmaceutical, food, environmental, and clinical testing industries. As India continues to strengthen its position as a global manufacturing and export hub, the next decade of HPLC evolution will increasingly be shaped not only by sensitivity and speed but also by sustainability.

Traditionally, analytical laboratories have consumed significant volumes of organic solvents such as acetonitrile and methanol while operating instruments continuously with high power demands. With growing emphasis on environmental responsibility, operational efficiency, and cost optimization, laboratories are now rethinking analytical workflows through the lens of green chromatography.

These systems enable faster analysis with lower solvent consumption, reducing both chemical waste generation and operating costs. Shorter run times also translate into lower energy usage per analysis, improving laboratory productivity while supporting sustainability goals.

In India, this shift is particularly relevant for pharmaceutical companies serving regulated markets such as the US, Europe, and Japan. Global customers and regulatory agencies are increasingly encouraging environmentally responsible manufacturing and testing practices. Laboratories that reduce solvent usage, improve energy efficiency, and minimize waste disposal burdens are likely to gain both economic and strategic advantages.

Automation is another key contributor to sustainable laboratory operations. Advanced system monitoring, automated shutdown modes, and intelligent workflow management help reduce unnecessary instrument idle time and optimize resource utilization. Improved reproducibility minimizes the need for repeat analyses, thereby indirectly reducing solvent and sample consumption.

Importantly, green analytical practices do not mean compromising analytical performance. Modern HPLC and UHPLC platforms are now capable of delivering higher throughput, enhanced sensitivity, and improved robustness while using significantly fewer resources than conventional systems.

As Indian laboratories continue to modernize their infrastructure, sustainability will become an increasingly important consideration in purchasing and operations. The future of HPLC in India will therefore not be defined solely by faster separations or higher sensitivity, but by how efficiently laboratories can achieve reliable analytical results with lower environmental impact.

In many ways, the next phase of chromatography evolution will be measured not only in peak resolution, but also in responsible resource utilization.

For Indian buyers, leverage has rarely been higher: better price-to-performance, richer service contracts, flexible financing, and faster local support. The medium-term consequence is vendor margin erosion, accelerated migration toward UHPLC and LC-MS where margins are still defensible, and an intensifying battle for the real long-term prize – aftermarket revenue from columns, consumables, software, and qualification services tied to a rapidly expanding installed base.

India’s emergence as a GLP-1 hub is the single biggest structural tailwind for the HPLC market over the next five years, sitting atop the broader generics and biosimilars story rather than replacing it.

GLP-1 receptor agonists – semaglutide, tirzepatide, liraglutide, dulaglutide – have become the defining therapeutic class of the decade. Novo Nordisk and Eli Lilly together cannot meet global demand even after massive capacity expansions, and the market is forecast to exceed USD 150 billion by the early 2030s. This persistent supply-demand gap, combined with patent expiries in emerging markets, is drawing the innovators toward India. Semaglutide’s Indian patent expires in March 2026, effectively setting off a wave of generic and biosimilar launches. Liraglutide is already off-patent, with multiple domestic versions on the market.

India’s peptide manufacturing credentials make it the natural partner. Biocon, Sun Pharma, Dr. Reddy’s, Cipla, Lupin, Zydus, and Aurobindo have all signaled GLP-1 ambitions. Innovators are pivoting from “defend” to “participate”: Eli Lilly has expanded its footprint in Hyderabad and Bengaluru and is exploring CDMO tie-ups for emerging markets, while Novo Nordisk is engaging with Indian partners for fill-finish and potentially API stages. The logic is to share the post-patent market rather than cede it entirely.

For HPLC vendors, the implications are exceptional. Peptide drugs are far more analytics-intensive than small molecules. A single semaglutide batch requires extensive HPLC and UHPLC work for peptide mapping, impurity profiling, deamidation and oxidation analysis, counter-ion content, residual solvents, and stability testing – typically multiples of the chromatography load per kilogram of API compared to a small-molecule line. Reverse-phase, size-exclusion, and ion-exchange HPLC are routinely used, often coupled with mass spectrometry.

The result is that every Indian player entering GLP-1 – plus CDMOs like Syngene, Piramal, Sai Life, Aragen, and Neuland, positioning for innovator partnerships – is simultaneously placing significant orders for HPLC, UHPLC, and LC-MS systems, along with columns, consumables, and qualification services. Layer on the broader biosimilars pipeline in mAbs, insulins, and fusion proteins, and the next-generation pipeline of oral GLP-1s and molecules like retatrutide, CagriSema, and orforglipron, and the trajectory is clear.

India is not just growing because the West has slowed. It is a market where analytical intensity per dollar of pharma output is rising, driven by the shift from small molecules to peptides and biologics. GLP-1 is the most visible expression of that shift today – and what is making India strategically indispensable to both innovators and the instrument vendors serving them.

In cost-sensitive Indian QC labs, the ROI calculus is shifting decisively away from mass spectrometry and toward multiplexed HPLC.

The economics are stark. An LC-MS/MS runs 200,000 to 500,000 dollars, high-res Orbitraps and Q-TOFs cross a million, and both carry steep service, consumables, and specialist-talent costs. A fully configured UHPLC with a high-end detector – DAD, fluorescence, ELSD, or charged aerosol – lands at 40,000 to 80,000 dollars and runs on widely available chromatography talent. For QC labs running compendial methods on 200 to 400 samples a day, MS rarely earns its CapEx.

Multiplexing amplifies the advantage. Parallel HPLC architectures from Agilent, Shimadzu, Waters, and Thermo run multiple independent streams from shared sample handling. Staggered-injection setups interleave columns on a single detector to double or triple throughput. 2D-LC replaces MS confirmation for many impurity-profiling and peptide applications. Charged aerosol and ELSD detectors have closed most of the historical gaps where MS was the only option.

The Indian context fits this perfectly. Compendial QC methods are HPLC-UV-based; generics demonstrate equivalence with conventional chromatography; and even peptide and biosimilar release can largely be handled by well-designed HPLC. The result is a clear preference to invest less in mass spectrometers, thereby saving CapEx and operating costs and expanding multiplexed HPLC capacity instead.

For HPLC vendors, this substitution effect is unambiguously positive – pushing demand toward higher-end UHPLC, advanced detectors, parallel architectures, and sophisticated chromatography data systems. The competitive message is shifting from peak instrument specs to total cost of analysis, and India is leading that shift.

India’s demand engine ignites

The single largest driver of demand is diabetes. India is home to an estimated 101 million people with diabetes and another 136 million with prediabetes, according to the ICMR-INDIAB study. Each diagnosed patient ideally requires HbA1c testing every three to six months, translating into hundreds of millions of glycated haemoglobin tests annually. As hospital chains and pathology networks chase NABL-grade standardization, HPLC has emerged as the preferred reference method–superior to immunoassay-based alternatives in resolving haemoglobin variants and analytical interferences.

Cancer is the second growth axis. India reports approximately 14.6 lakh new cancer cases each year, with incidence projected to rise nearly 12 percent by 2025 (ICMR-NCDIR). Expanding oncology services, adoption of biologics, and personalized therapy regimens are driving demand for therapeutic drug monitoring (TDM), biomarker analysis, and metabolite profiling–domains where HPLC delivers the precision required to fine-tune dosing and reduce adverse events. Cardiology, critical care, and infectious-disease management are following close behind.

A third tailwind is the rapid corporatization of diagnostics. The organized chains, Dr Lal PathLabs, Metropolis, SRL, Thyrocare, and Agilus now process tens of millions of samples annually and continue to consolidate market share. For these players, throughput, automation, and multi-shift uptime are board-level priorities. Modern HPLC systems, with high-capacity autosamplers and digital workflows, fit squarely into that operating model.

Finally, regulatory pressure is rewriting purchase criteria. Mandatory NABL accreditation, sharper CDSCO oversight, and the rising bar of customer expectations are pushing labs toward instruments that deliver reproducibility on paper and in audits. The cumulative effect–HPLC has shifted from good to have diagnostic equipment to a strategic, ROI-anchored investment.

Global market – A USD 46-billion runway

The global HPLC instruments market was valued at USD 22.45 billion in 2025, and is expected to reach USD 46.41 billion by 2035, expanding at a CAGR of 7.53 percent over the period, according to Market Research Future. That trajectory places HPLC among the most resilient segments in the analytical instruments space, even as broader life-sciences capex faces tighter scrutiny.

Three forces are doing the heavy lifting. First, regulatory intensity continues to climb. Agencies including the US FDA, EMA, WHO, and India’s CDSCO are tightening standards on data integrity, method validation, and impurity profiling–pushing laboratories toward high-precision, fully traceable analytical platforms. Second, the commercial pipeline has shifted. Personalized medicine, biologics, biosimilars, antibody–drug conjugates, and complex formulations are outgrowing traditional small-molecule analytics, accelerating demand for advanced HPLC and hybrid LC–MS systems. Third, automation, AI-enabled data analysis, portable systems for decentralized testing, and green chromatography are unlocking new use cases beyond core regulated industries.

Policy tailwinds compound the opportunity. Initiatives such as Make in India, the Production Linked Incentive (PLI) scheme for pharmaceuticals and medical devices, and rising healthcare R&D allocations across emerging economies are strengthening lab infrastructure and improving access to high-end systems. India’s medical device market alone is projected to grow from roughly USD 14 billion in 2024 to USD 50 billion by 2030, creating a deep secondary pull for analytical platforms.

Yet headwinds are equally real. Capital intensity remains high – a fully configured branded HPLC unit typically ranges from ₹20–85 lakh (USD 25,000–100,000), while LC–MS platforms can exceed ₹2 crore (USD 250,000), often rising by 15–25 percent after import duties, GST, and installation. Local and refurbished systems offer lower entry points but rarely meet the specifications required by NABL-accredited and regulated environments. Recurring costs – solvents, columns, and annual maintenance contracts – typically run 50–80 percent of acquisition value over a five-year horizon, a meaningful drag on lab P&Ls. Compounding the issue, India faces a chronic shortage of trained chromatographers, especially outside metro hubs. Competitive technologies such as standalone GC and MS, as well as tighter compliance requirements, also create friction.

The competitive response is reshaping the industry. Agilent Technologies, Waters Corporation, Shimadzu, Thermo Fisher Scientific, and PerkinElmer–who collectively command an estimated 70 percent of the global market–are doubling down on AI-driven platforms, sustainable consumables, and localized supply chains. In 2026 and beyond, expanding distribution networks, building compact, user-friendly systems, integrating cloud-based analytics, and forging service-led partnerships will determine market share. Hardware is no longer the moat. The combination of hardware, software, service, and consumables–delivered as a unified offering–is.

Diagnostics finds its gold standard

In Indian clinical diagnostics, HPLC has quietly become the gold standard. Its core value–accurate separation, identification, and quantification of compounds in complex biological samples–translates directly into better clinical decisions and stronger regulatory standing.

Diabetes care is the flagship use case. HPLC delivers the most precise, standardized, and reproducible HbA1c results available at scale, capable of detecting haemoglobinopathies and analytical interferences that confound immunoassay platforms. For an Indian laboratory chain that reports hundreds of thousands of HbA1c tests every month, even a marginal improvement in accuracy and turnaround time translates into meaningful brand differentiation and physician loyalty.

Beyond glycated haemoglobin, HPLC plays a critical role in identifying haemoglobinopathies, neonatal disorders, amino-acid abnormalities, and inherited metabolic diseases–conditions where early and accurate diagnosis dramatically alters lifetime outcomes and cost of care. India’s high prevalence of haemoglobin disorders, including sickle-cell disease and thalassemia, makes this capability strategically important; the National Sickle Cell Anaemia Elimination Mission alone aims to screen 70 million people by 2047.

In toxicology and therapeutic drug monitoring, HPLC quantifies drugs, metabolites, and toxins with precision that supports both clinical safety and forensic admissibility. Increasingly, it is also the workhorse behind biomarker testing and precision medicine, particularly in oncology, cardiology, and advanced clinical biochemistry.

The combination of automation, reliability, and diagnostic versatility has positioned HPLC as a future-ready platform for modern healthcare laboratories. The strategic question for buyers is no longer whether to invest, but which configuration delivers the strongest five-year ROI.

HPLC vs UHPLC – Choosing the right buying lane

As labs push for faster, more reliable testing, the HPLC vs UHPLC choice comes down to volume, turnaround needs, and cost. HPLC remains the dependable, lower-cost option (USD 25,000–60,000), ideal for routine testing in hospitals and mid-sized labs with steady workloads. UHPLC offers higher speed and efficiency, with up to 70 percent faster runs, lower solvent use, and better throughput–often delivering payback within 24–36 months for high-volume labs. However, it requires higher upfront investment (USD 60,000–150,000), specialized consumables, and method revalidation.

In practice, HPLC suits stable, cost-sensitive operations, while UHPLC fits scaling labs needing speed and productivity. Many networks now use a hybrid approach–HPLC for routine work, UHPLC for high-end analysis.

Hardware that drives performance

Modern HPLC buying decisions move well beyond headline specifications. Hardware architecture now directly determines speed, reliability, and long-term scalability–and increasingly, total cost of ownership.

High-performance pumps with stable quaternary-gradient capability enable precise solvent blending and greater method flexibility, while advanced autosamplers with low-carryover injectors safeguard accuracy in high-throughput environments where cross-contamination can compromise dozens of results in a single sequence. Column ovens with tight temperature control (±0.1 °C) improve reproducibility and peak consistency, especially for sensitive clinical assays where regulatory acceptability hinges on retention-time stability.

Equally critical is the shift toward modular systems and flexible preparative platforms, which allow laboratories to upgrade individual components, scale workflows, and adapt to evolving applications without replacing the entire instrument. For growing labs, contract research organizations, and academic centres, this modularity translates directly into better ROI, reduced downtime, and a longer useful life of capital. A well-chosen modular platform can extend its productive lifecycle from the industry-standard seven years to ten or more.

Once hardware architecture is defined, the next strategic decision becomes the differentiator–choosing the right detection strategy.

Detectors define differentiation

Modern HPLC buying goes beyond specs–hardware design now drives performance, reliability, and total cost.

Advanced pumps, low-carryover autosamplers, and precise column ovens improve accuracy, reproducibility, and throughput in demanding workflows. At the same time, modular systems let labs upgrade components, scale operations, and extend instrument life beyond seven years, improving ROI and reducing downtime.

Once the hardware is set, the key differentiator shifts to selecting the right detection strategy.

Where specialty testing grows

HPLC is expanding beyond routine diagnostics into oncology, cardiology, and specialty care. It supports drug monitoring, biomarker analysis, and lipid profiling–improving treatment precision and early diagnosis, especially in high-burden areas like cancer and cardiovascular disease.

It also plays a key role in nutrition, metabolic disorders, and personalized medicine, including biologics and pharmacokinetic studies.

As testing complexity and volumes rise, labs must adopt automation, integrated data systems, and high-throughput workflows to stay efficient and scalable.

AI enters the lab floor

AI is transforming HPLC into smart, self-optimizing systems. It accelerates method development from weeks to days, automates peak analysis, and detects errors in real time–reducing manual effort and improving data reliability.

Predictive maintenance is a key advantage, cutting downtime by 30-50 percent and boosting productivity in high-volume labs. End-to-end automation further streamlines workflows, enabling faster, more consistent results.

With rising workloads and limited skilled staff, AI is becoming essential–amplifying expertise, improving efficiency, and setting a new baseline for competitive laboratories.

Automation solves the talent gap

India’s chromatography market is growing fast, but a 30-40 percent talent gap–especially outside metros–limits consistency and scalability.

AI-powered HPLC is addressing this by automating method development, analysis, and error detection, reducing reliance on expert operators. Labs can standardize outputs across networks, cut training time from months to weeks, and improve accuracy.

The result is faster, more scalable operations, with smaller labs achieving near-reference standards–bringing advanced analytics to Tier-II and Tier-III markets.

Green labs, lean costs

Green chromatography is shifting from optional to essential, cutting solvent use, waste, and cost per test–often by 30–60 percent through optimized methods and safer alternatives like ethanol or CO₂.

For labs, this means lower operating costs, improved safety, and stronger ESG credentials, now a key procurement factor for large chains. Energy-efficient systems and smarter workflows further reduce environmental impact without sacrificing performance.

Overall, it delivers both economic and strategic gains–less compliance burden, better sustainability metrics, and long-term operational efficiency.

Beyond price – The true ROI of HPLC

The true cost of an HPLC system lies in total cost of ownership, often 2.5–3× the purchase price over five years.

Beyond CapEx, expenses include maintenance (8–12 percent annually), consumables, software, validation, and downtime–all of which shape long-term ROI. Efficient systems can cut cost per test by 20–35 percent, while complex setups add training and compliance burdens.

Smart buyers look beyond price to performance, service support, sustainability, and scalability–since the lowest upfront cost rarely delivers the best long-term value.

A new playbook for OEMs and distributors

India’s growing chromatography market is creating strong opportunities across pharma, diagnostics, and food testing, with rising demand for cost-efficient, locally serviceable HPLC solutions. This opens space for Make in India systems, local manufacturing, and compact clinical platforms.

Refurbished instruments are gaining traction in Tier-II and Tier-III labs, while after-sales services–AMCs, maintenance, calibration, and training–are becoming key differentiators in a fast-growing USD 300–400 million market.

Consumables and software offer recurring revenue, with cloud-based and AI-enabled platforms emerging as the next growth area. The shift is clear: success will depend on delivering integrated solutions, not just hardware.

Roadmap to the 2030 lab

By 2030, HPLC labs will evolve into connected, intelligent ecosystems. Compact and portable systems will enable decentralized testing, while hybrid HPLC–MS platforms will support advanced clinical applications like precision medicine.

AI will drive method development, maintenance, and troubleshooting, with cloud-connected networks ensuring standardized, compliant operations across sites. Data will become actionable, supporting faster clinical and research decisions.

As automation expands, even smaller labs will access high-end capabilities. HPLC is shifting from a standalone instrument to a strategic, digitally integrated healthcare platform.

Second opinion