ECG Equipment

Electrocardiography – From signal snapshots to intelligent heart guardians

ECG evolves into AI-powered, connected intelligence–shifting from episodic diagnosis to continuous, predictive cardiac surveillance.

Electrocardiography tells an extraordinary story of evolution–an odyssey from primitive electrical scribbles to today’s intelligent, interconnected cardiac sentinels. Over a century ago, the first ECG readings captured faint whispers of the heart’s electrical rhythm through bulky contraptions tethered to ink-wielding machines. Those early analog giants–massive, mechanical, yet dependable–became the bedrock of modern cardiac diagnostics by revealing arrhythmias, ischemia, and hidden conduction malfunctions long before advanced imaging was conceived. For decades, clinicians deciphered roll-fed paper traces under fluorescent lights–tedious but invaluable checks of the human heart’s electrical code.

Then came the digital revolution. Electronics, computing, and signal-processing breakthroughs transformed clunky recorders into compact digital powerhouses–automated, networked, and integrative across care ecosystems. Early digital machines offered cleaner tracings, automated interval measurements, and electronic storage, turning what was once a transient strip of paper into a permanent, shareable clinical asset. Over time, connectivity matured – ECG carts and bedside monitors began talking to hospital information systems, cardiology information systems, and electronic health records, embedding ECG data inside the broader clinical narrative of each patient. Today’s systems–sleek, intelligent, and data-hungry–deliver near-instant analyses, synchronize with enterprise platforms, and stream cardiac intelligence to clinicians anywhere inside or outside the hospital.

The rise of algorithm-driven wearables marks a decisive paradigm shift. ECG has escaped the four walls of the hospital to live on wrists, adhesive patches, textile-based chest straps, and portable handheld hubs. Instead of a single snapshot captured in a controlled environment, the heart’s electrical story is now recorded across hours, days, or weeks in real-world settings–during work, sleep, travel, and exercise. Continuous monitoring replaces isolated readings; real-time alerts replace delayed, routine follow-ups. For patients with paroxysmal arrhythmias or intermittent symptoms, this represents a fundamental change in diagnostic yield and time to diagnosis.

We have entered the era of ECG 2.0–smarter, faster, endlessly connected. With cloud analytics, mobile integration, and AI-enhanced interpretation, ECG now represents not just diagnosis but continuous cardiac vigilance. Cardiologists command predictive insight, remote accessibility, and data-backed precision at a scale the pioneers of electrocardiography could never have imagined. What began as ink on paper has evolved into a digital nervous system for cardiovascular care, linking devices, clinicians, and patients into a constantly learning ecosystem.

Indian market dynamics

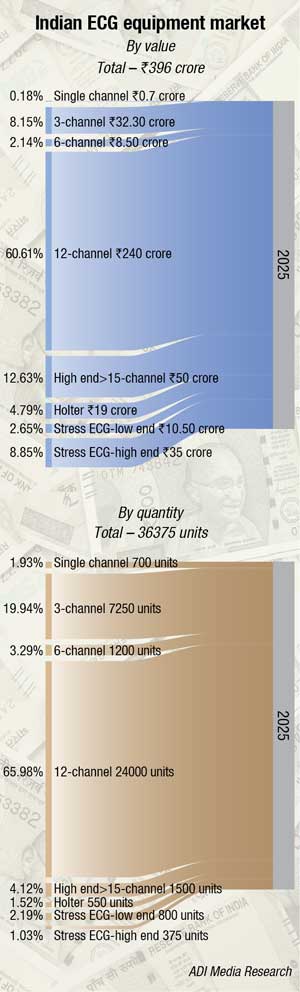

Indian market dynamics in ECG are shifting rapidly, with 2025 emerging as a pivot year from a hospital-centric installed-base market to a more distributed, digital and home-linked cardiac-monitoring ecosystem. The Indian ECG equipment market is valued at about ₹396 crore and 36,375 units in 2025 and is projected to grow at a compound annual rate of roughly 8.3 percent through 2031, on the back of rising cardiovascular disease, population ageing, lifestyle risk factors, and a stronger clinical and policy push for early diagnosis across care levels.

This demand backdrop is accelerating a visible technology shift toward portable, wireless and telemedicine-ready ECG systems, along with rapid uptake of AI-assisted and wearable solutions such as patches and Holter monitors, with Holter sub-segments, catered to primarily by Philips, GE, Schiller, BPL, Allengers, Edan, Contec and Spacelabs, expected to grow at above-20 percent CAGR through 2031. Usage is deepening not only in large hospitals and cardiology centers but also in smaller clinics and remote settings, as more affordable portable and connected ECG platforms integrate with telecardiology workflows and hub-and-spoke referral networks.

|

Leading players* |

|

| Tier I | BPL, and Schiller |

| Tier II | Philips, Nihon Kohden, and Contec |

| Tier III | Mindray, Allied, Comen, Allengers, Skanray, Nidek, Bionet, Mortara, Edan, and RMS |

| Others | Nasan, Medikit, Forest, Silverline Meditech, Omron and regional brands |

|

*Vendors are placed in different tiers on the basis of their sales contribution to the overall revenues of the Indian ECG equipment market. ADI Media Research |

|

On the supply side, India’s ECG landscape now settles into three distinct vendor tiers, spanning high-end hospital platforms to access focused digital devices. At the top, multinational vendors dominate the premium layer with high-spec cart systems, stress-test platforms and integrated cardiology or monitoring suites that are largely sold to tertiary centers and corporate hospital chains through bundled, multi-modality deals. The value-driven middle is led by domestic manufacturers offering complete ECG portfolios and dense service–dealer networks, with specific models often written directly into public tenders as de-facto benchmarks for Make in India, price-sensitive procurement in public institutions and nursing homes. A fast-growing third tier of health-tech companies is building pocket-sized, phone-connected and AI-assisted ECG devices for primary care, home monitoring and telemedicine, positioning themselves as the access and remote-screening front-end that can feed patients into hospital-based cardiology services.

Unchaining cardiovascular care – The shift to remote patient monitoring

Dr Amogh B Patil

Dr Amogh B Patil

Manager – Advanced Technology and Clinical Research,

Skanray Technologies Limited

For over a century, cardiovascular care has been anchored to the hospital bed–a reactive model relying on episodic data captured during brief clinical visits or acute emergencies. However, a profound shift is underway: driven by a looming cardiologist shortage and the escalating global burden of chronic heart disease, the medical field is rapidly transitioning from the bedside to the cloud.

At the heart of this revolution are next-generation electrocardiogram (ECG) systems. Moving beyond bulky Holter monitors and rudimentary consumer fitness trackers, today’s medical-grade smart patches utilize advanced nanomaterials and stretchable electronics. These strain-insensitive wearables offer unprecedented diagnostic fidelity, allowing high-risk patients to be continuously monitored in the comfort of their homes for weeks at a time. This continuous data stream captures transient arrhythmias and early signs of physiological deterioration that episodic care frequently overlooks.

Yet, continuous monitoring generates an overwhelming volume of data. To prevent physician burnout, modern telehealth architectures integrate robust artificial intelligence (AI). Advanced deep learning algorithms serve as a vital cognitive bridge, instantly parsing millions of heartbeats to filter out noise and elevate only clinically actionable alerts. Breakthrough AI models are already demonstrating the ability to detect severe acute events with greater accuracy than standard human triage, significantly reducing false-positive emergency activations.

For this ecosystem to truly succeed, interoperability is paramount. Cloud-based, vendor-neutral platforms seamlessly aggregate data from diverse proprietary devices directly into the provider’s Electronic Health Record (EHR). This bidirectional integration automates clinical documentation and billing workflows, reclaiming valuable time for physicians.

As cardiology decentralizes, safeguarding the remote care infrastructure against sophisticated cyber threats through decentralized learning and robust encryption remains a critical imperative. Furthermore, as we embrace algorithmic efficiency, we must ensure AI acts as an administrative savior–freeing doctors from computer screens–rather than a barrier that diminishes the human touch. By seamlessly connecting the patient’s home to the clinical cloud, next-generation ECG systems do not replace cardiologists; they empower them to deliver proactive, equitable, and deeply personalized care. These innovative solutions are urgently needed to maintain a seamless continuum of cardiac monitoring care, bridging the gap from the hospital to home.

Institutional ECG demand in 2025 was led by central institutes, state medical services corporations, and PSU hospitals, with most procurement routed through GeM and state e-tender portals, and more than 100 ECG machine tenders floated during the year. These were typically small-to medium-lot bids of about 5–15 units per site, heavily focused on tightly specified 12-channel trolley-mounted and PC-based systems for emergency, cardiology and general medicine departments, effectively turning ECG into a recurring, programmatic capital-expenditure line that supported mid-to high-single-digit market growth. Buyers ranged from apex and central government hospitals to state and municipal facilities, PSU hospital networks and academic and specialty centers, with tenders issued by institutions such as AIIMS campuses, large teaching and trauma centers, municipal corporations, state health departments and medical-services corporations for both stand-alone ECG lots and bundled cardiology or critical-care equipment packages.

Buyers included AIIMS, New Delhi, Bhopal, and Rishikesh; AMC General Hospital; MPPMCL Hospital, Jabalpur; Singareni Collieries Company Limited hospitals; Indian Institute of Science, Bangalore; and Apex Trauma Centre at SGPGIMS Lucknow. Bids have also been invited by Jamnagar Municipal Corporation, Puducherry Health Department, UP Health Department/SGPGIMS and Chhattisgarh Medical Services Corporation.

A key challenge for Indian ECG manufacturers is the influx of low-priced, finished machines imported from China, rebranded locally, and then marketed as Make in India despite minimal domestic value addition. These products often obtain all the necessary regulatory approvals, so they appear equivalent on paper but can be sold at prices that serious Indian manufacturers, who carry the cost of local R&D, tooling, and plants, find very hard to match.

Beyond the ECG cart – Patches, cloud, and the new economics of cardiac Monitoring

ECG and Holter monitoring are quietly shifting from expensive, box-based equipment to flexible, cloud-driven services that can run on low-cost devices and wearable patches. This turns ECG from a capital-intensive purchase into a predictable per-patient service with faster turnaround times and easier network-wide standardisation, with examples such as Tricog, Sunfox, and in-house hospital platforms.

Traditional ECG and Holter workflows were built around capital-intensive boxes: cart-based 12-lead ECG machines and standalone Holter systems for long-term rhythm monitoring. Hospitals and clinics would invest ₹1 lakh or more in a machine, pay for maintenance and consumables, and then rely on in-house or visiting cardiologists to interpret printed strips or local digital recordings. The economics were CapEx-heavy, utilization-sensitive, and largely confined to hospital premises. Holter monitoring, in particular, was a separate, relatively expensive process that used dedicated recorders and offline analysis software.

Over the past few years, this paradigm has begun to shift toward a service-centric model. On the hardware side, the emergence of wearables, 3-lead patches, compact, portable ECG devices, and phone-tethered recorders means that signal acquisition has become cheap, flexible, and location-agnostic. A 3-lead patch can be applied to a patient and worn for 24–72 hours, effectively replacing traditional Holter in many ambulatory monitoring scenarios. The provider charges a per-patient fee–typically in the ₹3,000–₹5,000 range for comprehensive long-term studies in India–covering device use, cloud storage, analysis, and reporting. Instead of buying and maintaining Holter recorders, hospitals can simply consume monitoring as a service. This lowers entry barriers for smaller centers and makes it easier to deploy monitoring at scale.

At the same time, low-cost ECG devices are widely available, including 12-lead variants that connect to smartphones or tablets. These devices focus on capturing a clean electrical signal from the patient, not on performing complex onboard analysis. Once the signal is digitized, it is transmitted to a cloud platform that handles interpretation. This decoupling of signal acquisition from analysis is fundamental: any compatible device–whether a branded cart, a Chinese low-cost ECG unit, or a phone-based recorder bought online in the ₹1,200–₹13,000 range–can act as a front-end sensor, while the real value resides in the cloud back-end.

Companies represent a mature, full stack implementation of this model. Their typical deployment in a clinic or small hospital consists of a basic ECG machine or communicator at the point of care, network connectivity, and a cloud platform that receives every tracing in real time. AI algorithms perform an immediate preliminary interpretation, flagging abnormalities, and a central team of cardiologists validates and finalizes reports within minutes. Clinicians at the periphery see a structured digital report on web or mobile, without needing local cardiology expertise or complex IT. Hospitals do not pay primarily for the hardware; instead, they pay per ECG (or via bundled packages), effectively turning ECG interpretation into a recurring service with defined turnaround time (TAT) commitments and quality metrics.

Growing importance of ECG data integration in connected healthcare systems

Akhil Kohli

Akhil Kohli

Director,

Allied Medical Limited

Electrocardiography has been one of the primary diagnostic tools in medicine for upwards of a century. It has been the cornerstone of measuring the heart’s electrical activity–detecting arrhythmias, myocardial ischemia, conduction abnormalities, and a wide range of cardiovascular conditions.

Traditionally, ECG devices have functioned as standalone diagnostic instruments in healthcare facilities. Its recordings were printed and stored manually or within the device. This meant that, more often than not, this crucial data remained siloed from the rest of the clinical information system, creating an inefficient workflow prone to manual errors.

This prompted the importance of ECG data integration in connected healthcare systems–from diagnostic endpoints to integrated components.

Aiming to build a continuous clinical record that’s accessible 24/7, ECG systems are now being integrated with Hospital Information Systems (HIS), Electronic Medical Record (EMR) systems, and enterprise cardiology platforms. This enables cardiologists, emergency physicians, intensivists, and surgeons to access cardiac data in real time.

Another dimension of this integration lies in the ability of ECG systems to communicate with other clinical platforms using technologies such as DICOM waveform. Adhering to these standards enables archiving the data within medical imaging systems that can be retrieved and shared across hospital networks with ease.

Portable ECG systems, wearable cardiac monitors, and remote telemetry platforms now enable cardiac signals to be captured outside traditional clinical settings and securely transmitted to central monitoring systems. By merging connected data with artificial intelligence, one can analyse waveforms and perform detailed comparisons to assist in the early detection of anomalies.

From Allied Medical’s perspective, this shift brings a mix of excitement and caution. We can foresee expanded design and implementation requirements to maintain a standard, effective way to integrate ECG data seamlessly. High-fidelity signal acquisition and diagnostic accuracy remain fundamental, but connectivity architecture, data management capability, and seamless system integration are now equally critical.

The fact remains that cardiovascular diseases (CVDs) are the leading cause of mortality. ECG data integration in connected healthcare systems has become a foundational requirement. The future lies where clinical precision, digital connectivity, and data centralisation intersect to equip healthcare professionals with faster access to patient information, efficient workflows, and deeper insights.

Sunfox, with its Spandan line and related devices, illustrates the hardware-plus-software side from a startup perspective. They offer ultra-portable, field-friendly ECG devices that plug into a smartphone and are priced low enough for use in small clinics, rural outreach, and even home settings. The device acquires multi lead ECGs, while the companion app and back-end algorithms handle analysis, alerting, and reporting. Again, the machine itself is not the main value; the analytical models, the user interface, and the ability to integrate with clinical workflows are. In effect, these companies are reframing the ECG machine from an expensive diagnostic asset to a commodity sensor attached to a powerful, continuously improving software brain.

Large hospital chains like Apollo are moving in a complementary direction by building their own central cloud software stacks and integrating ECG into broader digital health platforms. In such architectures, a hospital network may deploy relatively inexpensive ECG devices at multiple sites, route all traces to a centralized cloud environment where HIS/EMR, PACS, and cardiology viewers are co-located, and enable cardiologists to read from anywhere within the network. Once the core infrastructure is in place, the marginal cost of interpreting a single ECG drops sharply. It becomes plausible to run an internal ECG as a service model where per-patient internal cost could fall to tens of rupees, especially if they avoid external vendor interpretation charges and reuse existing cardiology manpower more efficiently.

This evolution is also transforming procurement behavior. Tenders are starting to move away from a narrow focus on ECG machine specifications, paper type, and warranty toward a focus on TAT, per-patient pricing, connectivity, and integration. For example, floating tenders can ask not which machine but what is your TAT and per-ECG charge for cloud interpretation and reporting, and which devices are supported. Hardware becomes almost incidental: hospitals can use BPL, Schiller, Skanray, Allied, or low-cost Chinese devices, or even devices they already own, as long as the vendor can ingest and interpret the data. Some providers offer to park their own compatible hardware in the hospital at low or zero CapEx, recouping costs via per-use charges. This is a reversal of the traditional model where hardware sales drove vendor revenue, and software was bundled free.

In this new landscape, cloud-based ECG software functions as a neutral backbone. It can accept data from many different front-end devices, normalize the input, run AI- and rule-based analysis, and present results in standardized formats. It also enables long-term storage, comparison across episodes, and cross-site access. For hospitals, the benefits are not just cost and convenience; they also gain audit trails, quality control, centralized analytics, and the ability to benchmark performance across their network. For vendors, the recurring revenue from per-ECG or per-patient charges is more predictable than episodic hardware sales and opens up new segments that would never have invested in high-end machines.

The clinical acceptance barrier, which historically centered on whether cardiologists would trust off-site or algorithm-assisted interpretation, is steadily eroding. As more cardiologists work with these systems, they see that the underlying signals are standard ECG tracings and that the clinical reasoning remains their own. AI is used as a triage and support tool, not a replacement. Once cardiologists are comfortable reviewing ECGs on digital dashboards rather than on paper, it becomes natural for them to read from home, at another hospital, or even on call, further detaching interpretation from the physical machine at the bedside. For patients, this can translate into faster diagnosis, especially in emergencies and in remote locations where immediate access to specialists was previously impossible.

For ambulatory monitoring and Holter-like use cases, patch-based wearables with 3-lead or more extended configurations are beginning to supplant traditional Holter recorders. These patches can continuously capture rhythm data for days, automatically upload it to the cloud via a gateway or a phone, and generate trend reports and event summaries without laborious manual downloads and offline analysis. The economics work best in a service model, where a provider charges per monitored patient, covering the device, connectivity, analysis, and reporting. Hospitals are relieved of the burden of buying and maintaining a dedicated Holter fleet and software, while still able to offer long-term monitoring with cardiologist-grade reporting.

Overall, the ECG and Holter segment is being redefined along three axes: first, hardware is being commoditized and pushed toward cheaper, smaller, and more flexible devices, including wearables and phone-based recorders; second, cloud software and AI are assuming the central role in analysis, workflow, and data management; third, the business model is shifting from capex-heavy equipment sales to per-patient, per-ECG, or subscription-based services. Once cardiologists accept that the clinical inference remains under their control and that cloud-mediated ECG is reliable, the system scales quickly. ECG acquisition can happen in a remote PHC, a small nursing home, or a patient’s home, while interpretation is centralized, standardized, and trackable. In that world, the box is almost irrelevant; what matters is connectivity, turnaround time, clinical quality, and how seamlessly the service plugs into the hospital’s or clinic’s overall care pathway.

Global scenario

This technological transformation is mirrored by the market’s expansion. The global ECG market, valued in the low tens of billions of US dollars in 2025 and projected to more than double by the mid-2030s, is riding a powerful wave of demographic, epidemiological, and technological drivers. Cardiovascular diseases–heart attacks, heart failure, arrhythmias, and cardiomyopathies–remain the world’s leading cause of mortality and morbidity. As populations age, lifestyles become more sedentary, and metabolic risk factors proliferate, health systems are compelled to identify cardiac threats earlier and manage them more intensively over longer lifespans.

Within this context, ECG occupies a unique position. It is non-invasive, relatively low-cost, and deeply embedded in clinical workflows across emergency departments, outpatient clinics, operating rooms, intensive care units, and community health settings. It serves as the first-line diagnostic weapon in chest pain evaluation, rhythm assessment, pre-operative workups, and routine health checks. As patient volumes rise and guideline-based care emphasizes early detection and longitudinal follow-up, the number of ECG recordings per patient and per episode of care is growing steadily.

The market itself is segmenting and stratifying. Traditional resting 12-lead ECG systems remain the backbone of hospital and clinic diagnostics, generating a substantial share of equipment and service revenue. However, faster growth is emerging in ambulatory monitoring, wearable patches, smartwatch-integrated ECG, and handheld point-of-care devices. On top of the hardware, an expanding software and services layer–ECG management systems, cloud-based storage, automated analysis, and AI-driven decision support–is becoming central to vendor strategies and provider procurement decisions.

AI infusion, cloud connectivity, and machine learning now amplify diagnostic speed and accuracy. Automated systems detect electrical anomalies with unprecedented precision, empowering clinicians to act before cardiac chaos unfolds. The traditional hospital-centric model is giving way to decentralized, always-on cardiovascular surveillance–bolstered by portable devices, home-based monitoring kits, and ubiquitous broadband connectivity. Many stakeholders now view ECG not merely as a piece of diagnostic equipment but as a recurring revenue platform, where analytics, tele-reporting, and managed monitoring services generate ongoing value.

Key drivers include the global surge in cardiovascular disease prevalence, geriatric population growth, sedentary lifestyles, and policy-backed preventive care initiatives. Governments and insurers are rolling out reimbursement frameworks and mass screening programs that embed ECG testing deep into public health infrastructure. From national atrial fibrillation detection campaigns to routine ECG incorporation in primary care screening bundles, ECG is shifting from episodic use to population-scale surveillance. As this happens, demand for standardized, scalable, interoperable ECG solutions accelerates across both mature and emerging markets.

Policy powerhouses and emerging economies

Policy ecosystems across Asia, Europe, and the Americas are increasingly decisive in shaping ECG adoption curves. In high-income countries, aging populations and high CVD burdens have prompted policymakers to prioritize early detection of arrhythmias, ischemia, and heart failure, leading to broader reimbursement for diagnostic ECG, ambulatory monitoring, and remote cardiac services. Updated clinical guidelines in various regions either recommend or strongly support extended ECG monitoring for stroke prevention, post-acute coronary syndrome follow-up, and evaluation of unexplained syncope or palpitations.

Governments are investing aggressively in telemedicine, rural digital infrastructure, and cloud-based cardiac monitoring systems. National telehealth programs are incorporating ECG as a core signal, enabling health workers in remote clinics to capture and transmit ECG recordings to centralized reading hubs or tertiary care centers. This is particularly visible in emerging markets, where cardiology specialists are concentrated in urban centers while rural populations bear a substantial share of the disease burden.

In countries such as India, Indonesia, Brazil, and others across Latin America and Southeast Asia, state-funded healthcare digitization and public–private partnerships are broadening access to ECG. Procurement frameworks and incentive schemes encourage primary care facilities and district hospitals to deploy digital ECG machines tied to telecardiology networks, dismantling affordability barriers that previously limited access to advanced diagnostics. These initiatives often align with national health insurance expansions and universal health coverage programs, making ECG part of reimbursable, standardized care pathways rather than an ad hoc add-on.

Regulators, meanwhile, are tightening safety and performance benchmarks, incentivizing research and development into precision sensors and validated AI algorithms. Updated standards relate not only to basic signal quality and device safety but also to cybersecurity, interoperability, and the validation of software-based interpretation tools. Regulatory scrutiny on AI models–covering training data, bias, explainability, and real-world performance monitoring–is becoming more rigorous. These interventions raise diagnostic fidelity and build clinician and patient trust, while also energizing innovation pipelines and fuelling collaborations among MedTech giants, AI startups, and hospital networks that can generate and curate high-quality datasets.

Collaboration surge and industry alliances

Strategic collaborations are now the ECG market’s rocket fuel. The era of single-vendor, standalone ECG boxes is giving way to multi-stakeholder platforms that join hardware, software, data analytics, and clinical services. Device manufacturers increasingly align with data analytics firms and AI developers to embed advanced interpretation algorithms directly into their systems or to offer seamless cloud-based analysis as part of their value proposition. Rather than relying solely on in-house development, many companies are pursuing co-development and licensing models that let them plug proven AI engines into existing product lines.

Partnerships with hospital systems and academic research institutions play an equally vital role. Co-development initiatives are validating emerging algorithms on large, diverse, real-world ECG datasets, ensuring that models generalize across different populations, care settings, and device types. This clinical collaboration is critical for meeting regulatory expectations and for securing buy-in from cardiology communities that demand both high sensitivity and specificity in high-stakes use cases.

Telehealth and remote monitoring companies are also entering the ECG ecosystem, integrating device fleets, cloud analytics, and clinician workflows into subscription-based services. In some regions, remote ECG interpretation centers offer 24/7 reading, triage, and escalation services to smaller hospitals and clinics, supported by AI tools that prioritize urgent tracings. Payers, in turn, are beginning to explore outcome-based contracts where reimbursement is linked to reductions in stroke, hospitalization, or readmission rates achieved through systematic ECG-based monitoring.

Such alliances are likely to define the electrocardiography landscape through 2026 and beyond. Interoperability, data integration, and predictive modelling are moving from nice to have features to core selection criteria for health systems upgrading their ECG infrastructure. Vendors positioned as ecosystem orchestrators–rather than commodity hardware suppliers–stand to benefit the most.

AI and deep learning – The diagnostic engine

Artificial intelligence has redrawn the boundaries of ECG interpretation. For decades, automated ECG analysis relied on rule-based algorithms that measured intervals and amplitudes, flagged rate and rhythm abnormalities, and suggested provisional diagnoses. While useful, these systems were limited in their ability to recognize complex patterns or to provide prognostic insights beyond binary normal/abnormal classifications.

Deep learning has changed that calculus. Modern neural networks ingest raw or minimally processed ECG waveforms and learn to extract intricate spatiotemporal features that correlate with a wide spectrum of conditions. They are sensitive to the faintest waveform fluctuations–subtle P-wave morphologies, nuanced QRS fragmentation, ST–T segment deviations, and repolarization abnormalities–that human readers might overlook or interpret inconsistently, especially in time-pressured settings. These models do more than classify arrhythmias; they can detect left ventricular dysfunction, hypertrophic cardiomyopathy signatures, and patterns associated with ischemic heart disease, even in the absence of overt ECG abnormalities.

AI-driven ECG platforms feed on millions of annotated datasets, continuously refining pattern recognition across diverse populations. As training datasets expand to include patients across age groups, ethnicities, comorbidities, and device types, the robustness and generalizability of these models improve. The newest battle-ready algorithms are explicitly engineered to handle noisy signals, electrode inconsistencies, motion artifacts, and wearable data gaps while maintaining diagnostic potency. Preprocessing pipelines and data augmentation strategies help them learn to distinguish artifacts from genuine physiological signals.

Explainable AI enhances physician trust by visually mapping waveform segments of clinical interest–highlighting, for example, the specific QRS deflections or ST-segment deviations that drive a model’s inference. This allows clinicians to cross-check algorithmic output against their own expertise, transforming AI from a mysterious black box into an intelligible assistant. Integration into reporting software further streamlines workflows– Suggestions, probability scores, and risk estimates can be embedded directly into structured ECG reports, enabling faster yet more informed decision-making.

Lean, energy-efficient neural frameworks now deliver onboard analytics for wearables and portable recorders, achieving real-time edge computing while syncing with cloud diagnostics when bandwidth is available. This architecture democratizes access to advanced cardiac interpretation, enabling deployment of sophisticated analysis at rural telemedicine hubs, community health centers, and even patient homes, while reserving heavy computational tasks and periodic model updates to the cloud.

Prediction over reaction – ECG’s preventive edge

The transition from diagnosis to prediction defines ECG’s modern renaissance. Historically, ECGs were ordered in response to symptoms or as part of pre-defined protocols; they were reactive tools, capturing the heart at a moment in time and answering immediate clinical questions. AI-augmented ECGs are changing this paradigm by extracting prognostic signals that forecast the probability of heart failure, arrhythmias, or ischemic events–often years in advance.

Subtle shifts in electrical rhythm, changes in waveform shape, or patterns that appear normal to the human eye can encode early signs of structural remodelling, autonomic imbalance, or subclinical ischemia. When modelled at scale, these patterns become powerful predictors. A single 10-second ECG, for example, can reveal an elevated risk of developing atrial fibrillation or reduced ejection fraction, prompting proactive surveillance or further imaging. Serial ECG data, captured over time, can be used to generate individualized risk trajectories rather than static classifications.

This evolution aligns with the global pivot toward preventive, data-driven healthcare. ECG technologies, supported by telemedicine and portable form factors, empower clinicians to safeguard population segments before crises strike. Continuous long-term data streams–analyzed through advanced analytics–create patient-specific risk maps, fuelling proactive care rather than reactive management. Health systems can segment their populations into risk tiers, allocate resources more effectively, and design targeted interventions that reduce hospitalizations and adverse events.

In 2026, ECG ceases to be a momentary test; it becomes a real-time barometer of cardiovascular resilience. For payers and providers operating under value-based models, this predictive capability is not merely clinically attractive; it is financially strategic.

Wearable tech and telecardiology revolution

Wearable ECG systems have redefined mobility, convenience, and continuity in cardiac care. Modern ECG patches adhere comfortably to the chest for days or weeks, recording continuous rhythms with minimal disruption to daily life. Smartwatches equipped with ECG functionality allow users to capture single-lead tracings on demand when they feel palpitations, dizziness, or chest discomfort. Handheld and smartphone-connected recorders provide quick, point-of-need measurements in clinics, ambulances, or homes.

These devices deliver uninterrupted or near-continuous cardiac telemetry, identifying transient arrhythmias or ischemic hints unseen in traditional tests that last only a few seconds. They are particularly valuable for diagnosing paroxysmal atrial fibrillation, frequent ectopy, or conduction disturbances that might otherwise elude detection. Patient engagement rises as individuals gain the ability to trigger recordings during symptoms and review basic summaries of their readings, while clinicians gain access to richer, longitudinal datasets rather than isolated snapshots.

Paired with telecardiology, these advancements dissolve geographical and temporal barriers. Real-time or near-real-time transmissions connect patients from remote outposts to cardiologists in urban hospitals within seconds or minutes. Digital networks facilitate rapid triage of abnormal recordings, continuous follow-up of chronic patients, and longitudinal cardiac profiling that spans episodes of care and changes in therapy. Hospital congestion can be reduced as non-urgent assessments shift to virtual channels, and diagnostic delays shrink as ECG data arrives before the patient does.

Governments and NGOs increasingly deploy mobile ECG programs in community screening, workplace campaigns, and rural outreach to snare early-stage cardiovascular threats. By equipping primary care workers or mobile vans with portable ECG devices linked to tele-reporting hubs, health systems can extend specialized diagnostic capability to regions that previously lacked consistent access to cardiology services.

Sensor innovation and hybrid biosensing platforms

Next-generation ECG sensors now blend comfort, durability, and elite signal purity. Traditional gel electrodes and rigid leads are giving way to ultra-flexible, skin-friendly materials that contour with body movement and maintain stable contact without causing irritation. Textile-based electrodes integrated into vests or garments, and dry-contact sensor arrays, reduce preparation time and improve the patient experience, making long-duration monitoring more feasible.

Signal quality is simultaneously being elevated by advances in electronics and algorithms. High-input-impedance front ends, better shielding, and intelligent filtering help suppress noise from muscle activity, motion, and environmental interference. AI-driven noise suppression algorithms further refine waveforms, separating true cardiac signals from artifact clutter. Clean, high-fidelity signals not only improve human interpretation but also feed AI models with the consistent input they need to deliver reliable results.

The frontier expands further with hybrid biosensing platforms that merge ECG with real-time physiological and biochemical monitoring. Multi-sensor wearables can combine ECG with photoplethysmography, respiratory metrics, activity tracking, temperature, and, in some cases, emerging biochemical indicators. These systems deliver a unified picture of the body’s dynamic interplay–capturing not just heart rhythms but oxygen levels, metabolic fluctuations, autonomic tone, and stress biomarkers. Correlating electrical patterns with other physiological signals deepens insight into conditions like sleep apnea, exercise intolerance, and autonomic dysfunction.

Such platforms define the next level of personalized cardiovascular medicine. They transform the ECG from a single-channel diagnostic tool into a multi-dimensional wellness surveillance network, where contextual data enriches interpretation. Clinicians can distinguish benign rhythm variations from those occurring in the setting of hypoxia, fever, or intense exertion, and tailor interventions to the individual’s real-world physiologic context rather than isolated readings.

The future – Intelligent cardiology unleashed

By late 2026, intelligent cardiology is poised to anchor medicine’s digital core. ECG technologies–once standalone tests executed at a single point in time–are morphing into adaptive, learning ecosystems powered by AI, bioinformatics, and pervasive connectivity. Continuous heart data feeds integrate with electronic health records, laboratory results, imaging, genomics, and social determinants of health, turning every heartbeat into actionable intelligence embedded in the larger clinical picture.

This evolving infrastructure heralds a healthcare architecture built on foresight rather than hindsight. Smart ECG systems will not only signal trouble; they will anticipate it, recommend interventions, and evolve through machine learning feedback loops. Each new ECG recording, each confirmed diagnosis, and each outcome event becomes a data point that refines future risk estimates and enhances algorithmic accuracy. The leap from clinical monitoring to predictive cardiovascular guardianship stands among the decade’s most profound healthcare revolutions.

As AI grows more sophisticated and biosensors become more intuitive, ECGs become more than diagnostic instruments–they become the living interface between human biology and intelligent medicine. For clinicians, this means access to deeper, more timely insight without sacrificing efficiency. For health systems, it means the ability to manage cardiovascular risk across populations with unprecedented granularity. For patients, it means that the humble ECG, once a brief and often forgotten test, is evolving into a continuous ally–quietly watching, learning, and helping to guard the heart in real time.

Second opinion

AI-driven ECG equipment – Transforming cardiac care in India.